Two Minutes From the Bottom: My Hands Moved, My Principal Didn't

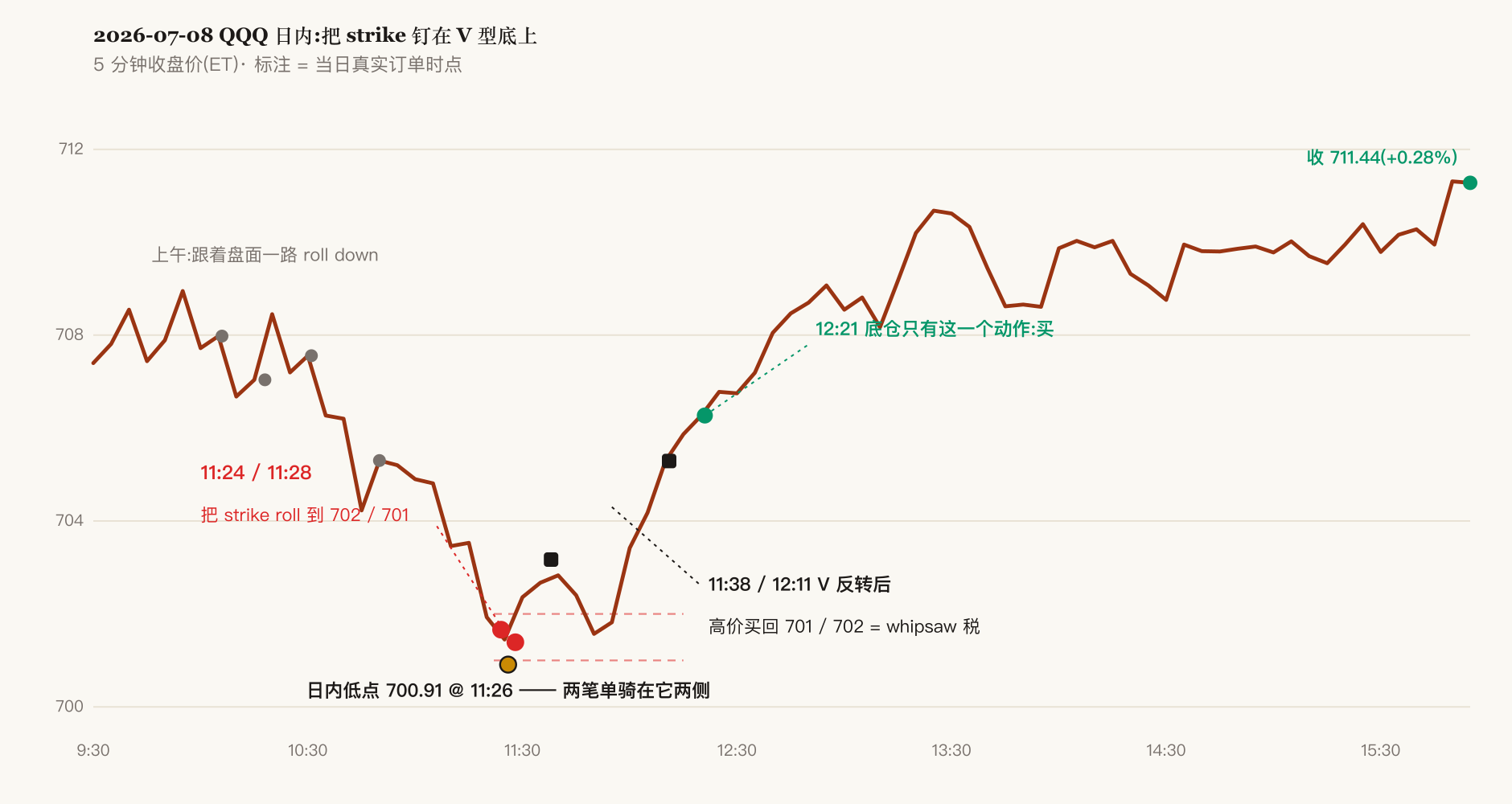

July 8, 2026, 11:24 AM Eastern: I rolled a batch of QQQ calls from the 715 strike down to 702.

11:26: the intraday low printed. 700.91.

11:28: I rolled another batch from 710 down to 701.

Two orders, straddling the exact low of the day by two minutes on each side. This isn't hindsight traced off a chart — it's broker order-flow timestamps matched against the one-minute tape. Forty minutes later the market V-reversed and closed at 711.44. The two strikes I had nailed to the floor, I bought back at higher prices at 11:38 and 12:11.

The conclusions up front, because this post-mortem has two honest sides:

| Question | Answer |

|---|---|

| Did the principal move? | Not one share sold. The stock core sat untouched through peak panic; at 12:21 I even added a little — the single most valuable fact of the two days |

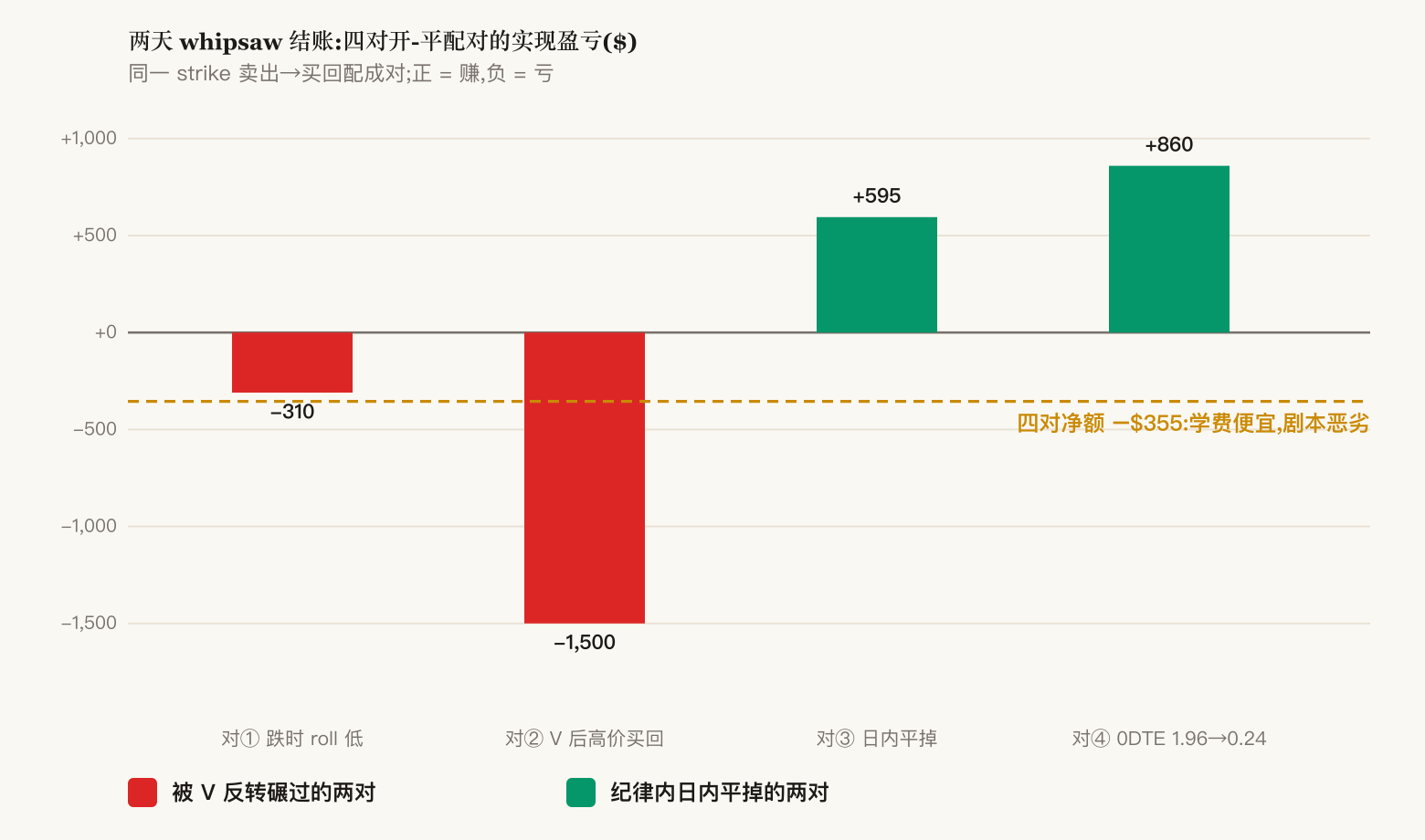

| Then where did it leak? | The options overlay: the same call line rolled repeatedly intraday; four open-close pairs settled −310 / −1,500 / +595 / +860 = net −$355 |

| Biggest mistake | Reactive intraday rolling, dragged by the tape — the last two rolls straddled the intraday low |

| The fix | ITM legs are now held to expiry, assigned, and rebuilt inside the expiry-day window; "intraday rolling" is deleted from the procedure entirely |

Cheap tuition, ugly script. The cheapness was luck; the ugliness is structural — and structure is what this post takes apart.

1. Timeline: how panic leads the hand

One sentence of backdrop: July 7, Middle-East escalation, with the previous day's "Samsung prints record profit, stock circuit-breaks anyway" panic still spreading. QQQ sold off hard for two days. My pre-market calibration to myself was three words: don't capitulate — because this kind of cascading decline is a meat grinder that can only reach three kinds of people: the leveraged who get margin-called, the pained who cut manually, and the screen-watchers with itchy hands.

Score: on the principal side, I passed. On the overlay, the itch won.

| Time (ET) | Action |

|---|---|

| 07-07 all day | Rolled down repeatedly into the decline; also swapped a dead strike on another single name into a rent-paying ITM one |

| 07-08 09:30 | QQQ opens 704.95, keeps probing lower |

| 10:06–10:50 | Four roll-downs, chasing the tape |

| 11:24 | 715C → 702C (same-day expiry) |

| 11:26 | Intraday low 700.91 |

| 11:28 | 710C → 701C; same ticket closes the 0DTE leg sold at 1.96 that morning for 0.24 |

| 11:38 / 12:11 | The V reverses; 701 / 702 bought back at higher prices — the whipsaw tax is realized in these two tickets |

| 12:21 | The core position's only action of the day: buy |

| 16:00 | Close 711.44 (+0.28%), White House walk-back plus chip-dip buyers |

Each ticket, in isolation, had a plausible intraday justification: the old strike carried pennies of extrinsic value, so not rolling meant zero rent; ATM theta density is the fattest, so rolling there collects the most. But string a dozen tickets together and you see one hand finding things to do inside a panic — every individually "reasonable" adjustment summing to chasing the tape in both directions.

2. Settling up: what the whipsaw tax looks like

Pair each strike's sell with its buyback across the two days and four pairs fall out:

Net −$355. The number itself doesn't hurt. But a post-mortem must account by behavior, not by outcome: the same behavioral pattern inside a deeper V produces a tax bill an order of magnitude larger. "It didn't cost much" is the most seductive bad news of these two days — it makes the error look forgivable.

3. Three mistakes — all mechanism, no feelings

1. Reactive intraday rolling = market timing in a costume. I had already sentenced my own timing ability to death by backtest: moving-average and momentum overlays, no statistically significant edge, confidence intervals straddling zero. But the word "roll" is camouflage — it sounds like position management, not timing. The fact is: any intraday action taken in response to price is timing. Making reactive intraday adjustments to a negative-gamma short-option book means paying the whipsaw tax in expectation — not bad luck, arithmetic.

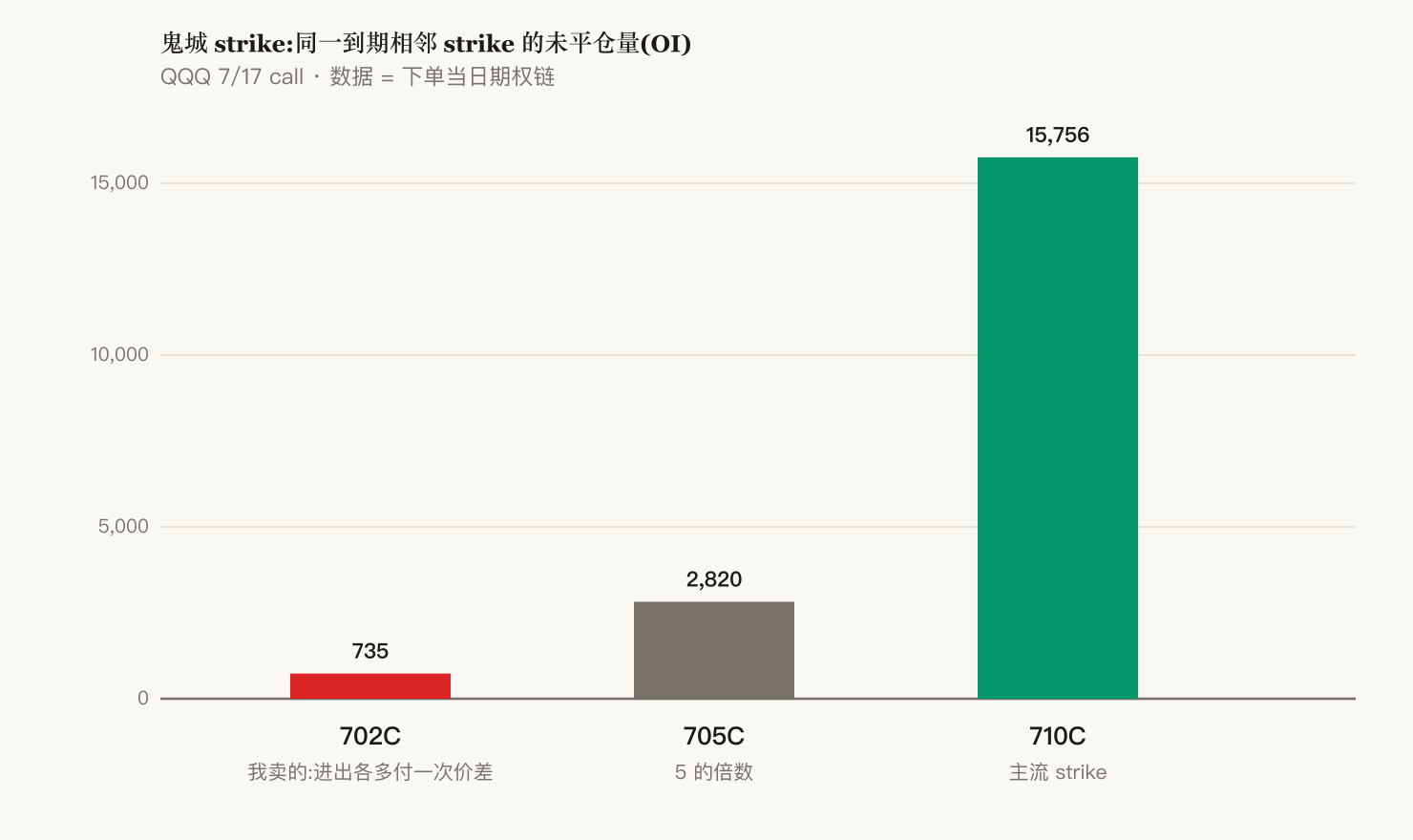

2. Selling ghost-town strikes. The 701 and 702 I sold in the panic are strikes nobody lives at:

3. Working the same line repeatedly in one day. Every touch costs two legs of friction, and the intraday oscillation nets most of it away by itself — several rounds of tolls paid for nothing but the feeling of doing something.

4. Three things done right (an honest post-mortem cuts both ways)

- Not one share of the core sold; added near the low. The only fact of the two days that truly matters. The grinder cannot wash out someone who doesn't need to sell — this time, on the principal side, my name wasn't on its list.

- The 0DTE leg obeyed the rules: sold at 1.96 in the morning, closed at 0.24 before the last hour, +$860. "0DTE legs must be closed before the close" executed cleanly.

- The motive for rolling down — harvesting theta — is sound. Swapping dead strikes for rent-paying ones points the right way. What failed was timing (reactive, intraday) and frequency (repeatedly, same day), not direction.

These three must be written down, and not as self-consolation: if the post-mortem records only errors, then in the next crash I'll start doubting the one rule that is life itself — don't sell the core.

5. The fix: delete the "should I act intraday?" decision itself

The three mistakes share one upstream cause: during market hours, I held decision rights. So the fix is not "stay calmer next time" — I've told myself that countless times to zero effect. The fix is to move the action out of market hours entirely, so the judgment call ceases to exist.

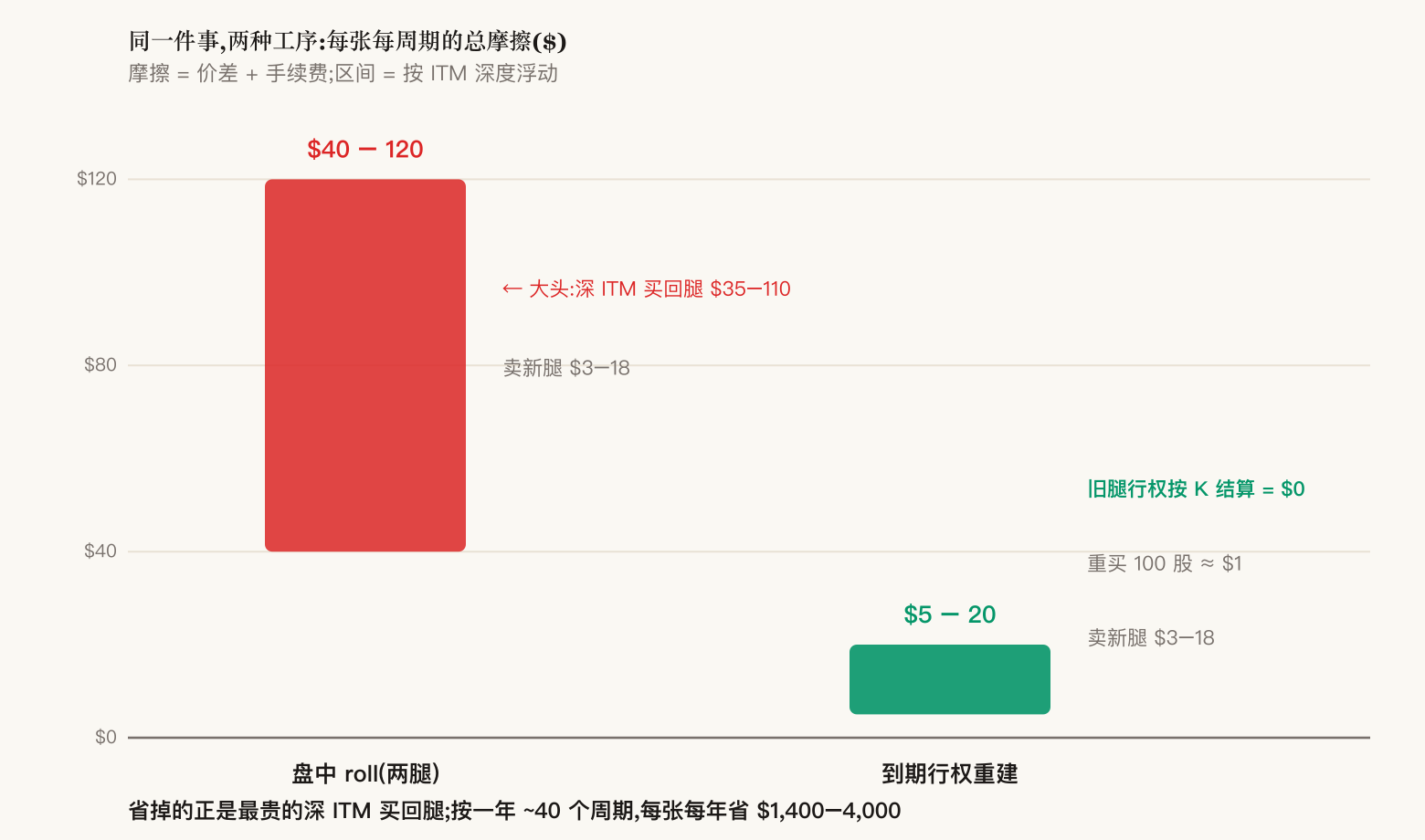

The procedure is called expiry-assignment rebuild. The arithmetic: an intraday roll pays two legs, and the expensive one is buying back a deep-ITM call. But if the old call is simply held to expiry and assigned — settled at the strike price — that most expensive leg's friction becomes zero:

| Path | Old call | Stock | New call | Friction per contract |

|---|---|---|---|---|

| Intraday roll (two legs) | Deep-ITM buyback, $35–110 | untouched | $3–18 | $40–120 |

| Expiry-assignment rebuild | Assigned at K = 0 | rebuy 100 shares ≈ $1 | $3–18 | $5–20 |

Both branches win: if the price finishes above the strike, the table above applies; if it finishes below, the old call expires worthless — no assignment, no friction at all. At roughly 40 cycles a year, that's $1,400–4,000 of friction saved per contract per year — multiply by your own contract count.

The boundary matters: this procedure governs only deep-ITM legs still carrying thick extrinsic value — held to expiry, they get to earn all of it. Out-of-the-money winners don't qualify; they keep their existing roll cadence.

But the savings are a byproduct. What the procedure actually buys is this: during market hours, I have nothing to do. The action is pinned to one window before the close on expiry day; in every other trading hour, "judgment" has no scene in my script.

6. Three seals

| This week's error | Seal | Nature |

|---|---|---|

| Reactive intraday rolls | ITM legs held to expiry; action fixed to the expiry-day closing window | Timing locked; intraday decision rights revoked |

| Ghost-town strikes | Sell only multiples of 5; quote maker prices from the engine's output, never chase | Selection delegated to liquidity data |

| Reworking one line repeatedly | On non-roll days, watch exactly one number: distance to forced liquidation. Never P&L | The input that produces "pain" is unplugged |

None of the three requires an intraday judgment — that is the design criterion, not a coincidence.

Coda

In the previous post I deleted every alpha-seeking component from the strategy, keeping only the beta core and survival constraints, and installed three mechanical gates: no opening on red days, a leverage-flag veto, a fixed trading window. These two days were that system's first live-fire test — report card: principal side, full marks; overlay side, failed.

The progress is that this time the root cause has a name: the mechanics are easy, the hard part is me — and "me" is most dangerous during precisely those minutes when I hold intraday decision rights. So the fix this time isn't yet another "resist harder" rule. It physically revokes decision rights from that time slot. Hands that don't itch aren't a sign of discipline; they're a sign the schedule contains no scene for them.

Rules are written in the calm after the close precisely so that nothing needs deciding during the session. The two orders placed two minutes from the intraday low are the most expensive footnote to that sentence I own — and mercifully, this edition came cheap.