Strategic Retreat: I Deleted Every Alpha Component From My Options Strategy

I deleted every "alpha-seeking" component from my own options strategy.

Not because I lost my nerve — because after testing with real money, the data told me those components never had any predictive power to begin with. This post is the story of that retreat: what got deleted, why, and what the remainder actually earns its keep with.

The old faith: selling volatility is "picking up free money"

Retail options circles run on a popular narrative: implied volatility (IV) persistently exceeds subsequently realized volatility (RV), and the gap — the volatility risk premium (VRP) — makes selling options like running an insurance company. Premiums collected exceed claims paid, forever. Free money.

I believed it, and more seriously than most. Not content with "index-level VRP is positive," I built a full single-name screening system: forecast each stock's future realized volatility with a HAR-RV model, compute "net VRP = IV − forecast RV − friction," sell vol on the names with the highest net VRP, buy vol on the most negative. In theory, this sharpened "free money" down to the individual stock.

Then I did two things most people never do: backtest the signal itself, and test it with real money.

The data came back. Two slaps.

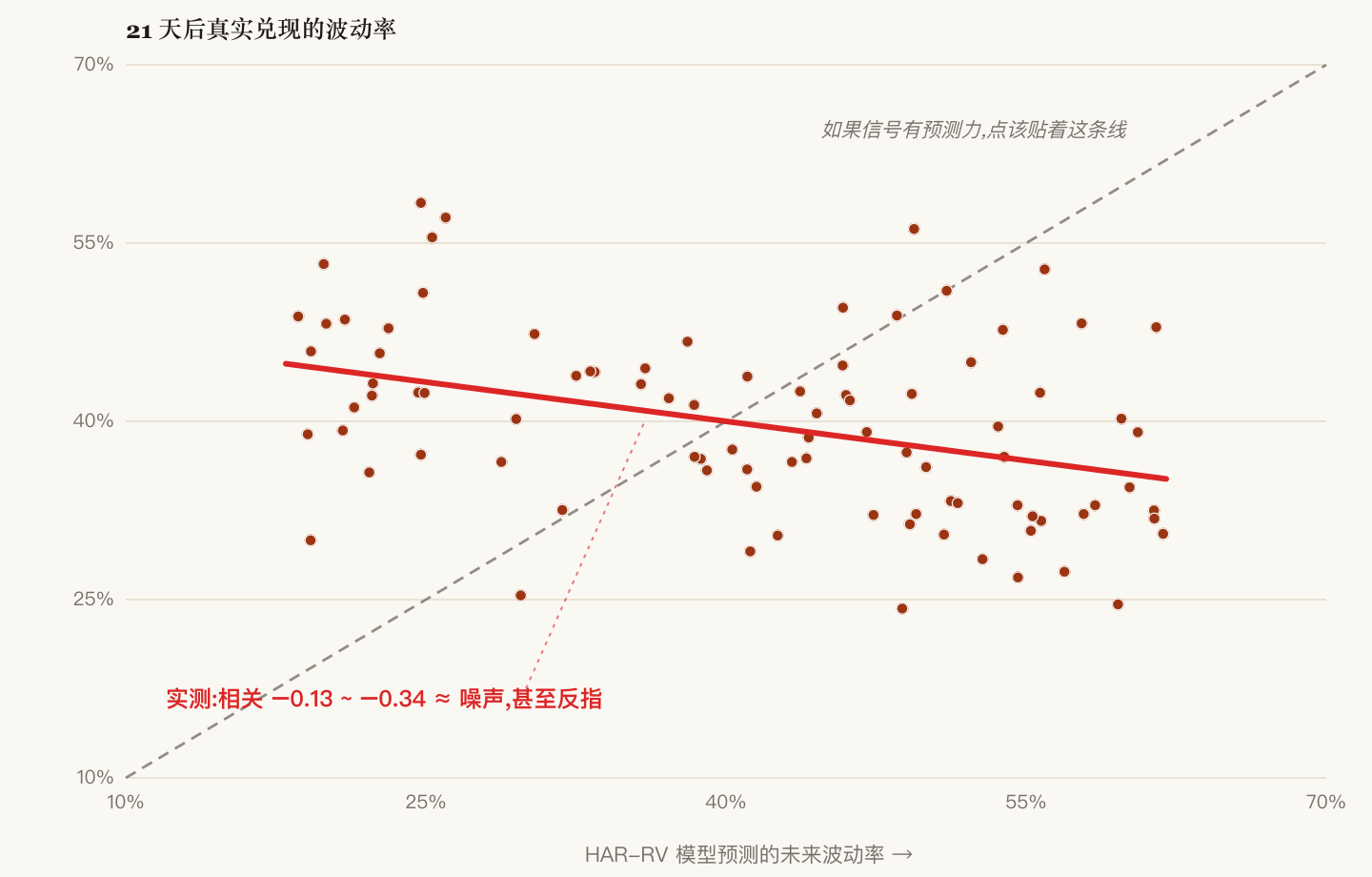

First slap: the signal is noise. The measured correlation between HAR-RV forecasts and volatility actually realized over the next 21 days: −0.13 to −0.34. Not "weakly positive" — near zero and pointing the wrong way. The level of "net VRP" carries no bettable information: a high reading means the market priced it high, not that you can capture it. The ruler I was ranking my bets with was a piece of noise.

Second slap: real-money validation, −4.5%, zero wins in five trades. I wired the signal to automated execution with a small live account. Five trades, five losses. Not bad luck — a zero-edge signal is supposed to produce exactly this.

Along the way I killed the adjacent routes too: long volatility (buying straddles) — no; index-level alpha — ruled out even earlier. A retail trader with no information edge, no market-making infrastructure, and no inside knowledge has roughly zero probability of out-pricing institutions in options. Unpleasant, but that's what the arithmetic says.

Where the retreat ends: a beta core plus survival sizing

After deleting all the alpha, what's left? Ironically, the only part of the strategy that ever stood up to scrutiny:

The only compounding engine = holding growth beta (index/growth equities) + survival sizing (a leverage cap plus margin stress tests, so you are never force-liquidated).

Unpacked, that's three plain facts:

- Beta is free. You need no forecasting skill to collect the market's return by holding a broad growth index. It is the only money a retail investor can collect without an edge.

- Leverage amplifies beta, not alpha. Moderate leverage can raise long-run returns, but it isn't skill — it's the price of risk.

- The only thing worth calling an edge is staying alive. I stress-tested my own book: at a bit over 2.2x leverage, the buffer to forced liquidation was roughly a −26% drawdown; at 3x, the buffer gets thin enough for one deep correction to punch through. Forced liquidation is the death penalty for compounding — it converts a recoverable drawdown into permanent loss, and it always triggers at the bottom. A leverage cap isn't a style preference; it's a survival constraint you compute from a stress test.

And options? Demoted to risk-control accessories. No longer a source of income:

| Tool | What it does | What it is not |

|---|---|---|

| Iron condor | Structurally caps the maximum loss per position | Not a "high-win-rate money printer" |

| Deep-ITM LEAP as stock (PMCC) | Downside floor + can-never-be-liquidated insurance | Not "cheaper financing" — full carry costs more than margin; the excess is the embedded put you're forced to buy |

| OTM covered calls | Small rent + smoother drawdowns | Not alpha: my own backtest puts risk-adjusted edge ≈ 0, confidence interval straddling zero |

Note the last row: even the covered call — the crown celebrity of retail options strategies — is not alpha on a risk-adjusted basis. It's legitimate, because it trades away the right tail for shallower drawdowns; but the "rent" you collect is, over the long run, exactly the upside you surrendered. Selling calls while knowing this, versus selling them believing you're picking up free money, are two entirely different psychological positions.

The most valuable lesson of the retreat: when you're losing, do nothing

With the strategy stripped clean, one question remains: what do you do when the call you sold gets run over? Every covered-call writer faces this eventually, and it's the scenario with the highest emotional damage — that call leg in your account bleeds red, daily.

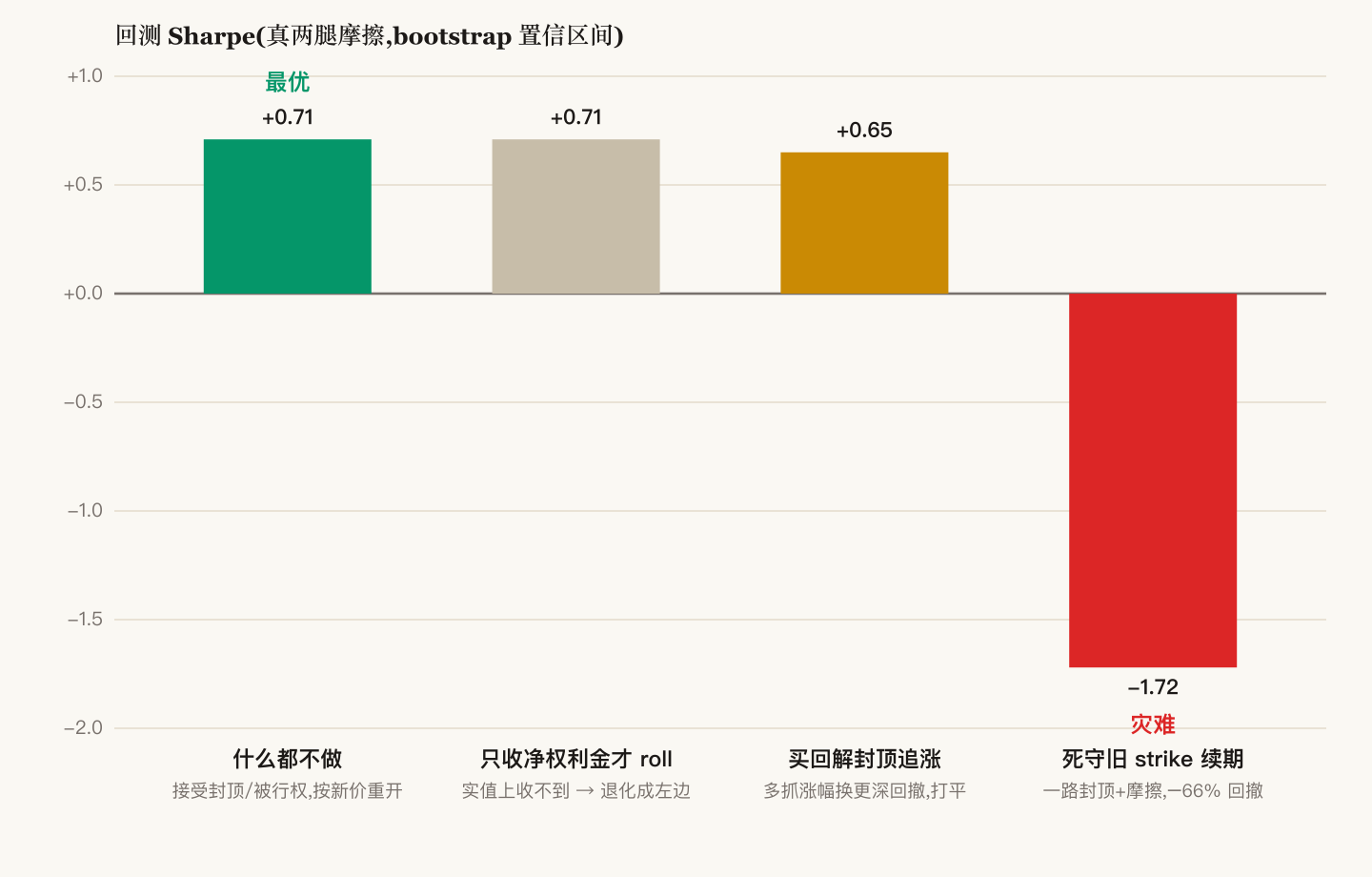

I ran a dedicated backtest: fix how the winning side is handled, vary only "what to do on the losing side," with real two-leg friction and bootstrap confidence intervals. Results:

| Losing-side strategy | Sharpe | Max drawdown | Verdict |

|---|---|---|---|

| Do nothing: accept the cap / let assignment happen, re-open at the new price next cycle | 0.71 | −31% | Optimal |

| Roll up-and-out (only when net credit) | 0.71 | −31% | Almost no net credit exists ITM → collapses into the row above |

| Buy back immediately, uncap, chase the rally | 0.65 | −32% | A bit more upside for deeper drawdowns and more friction; statistically a wash |

| Defend the broken strike, rolling it forward forever | −1.72 | −66% | Disaster: capped all the way up + churn friction, ending in liquidation |

Read that table carefully: the Sharpe-optimal action is "basically do nothing," while the action your account screams for — defend, stop the bleeding — is the only one that ruins you.

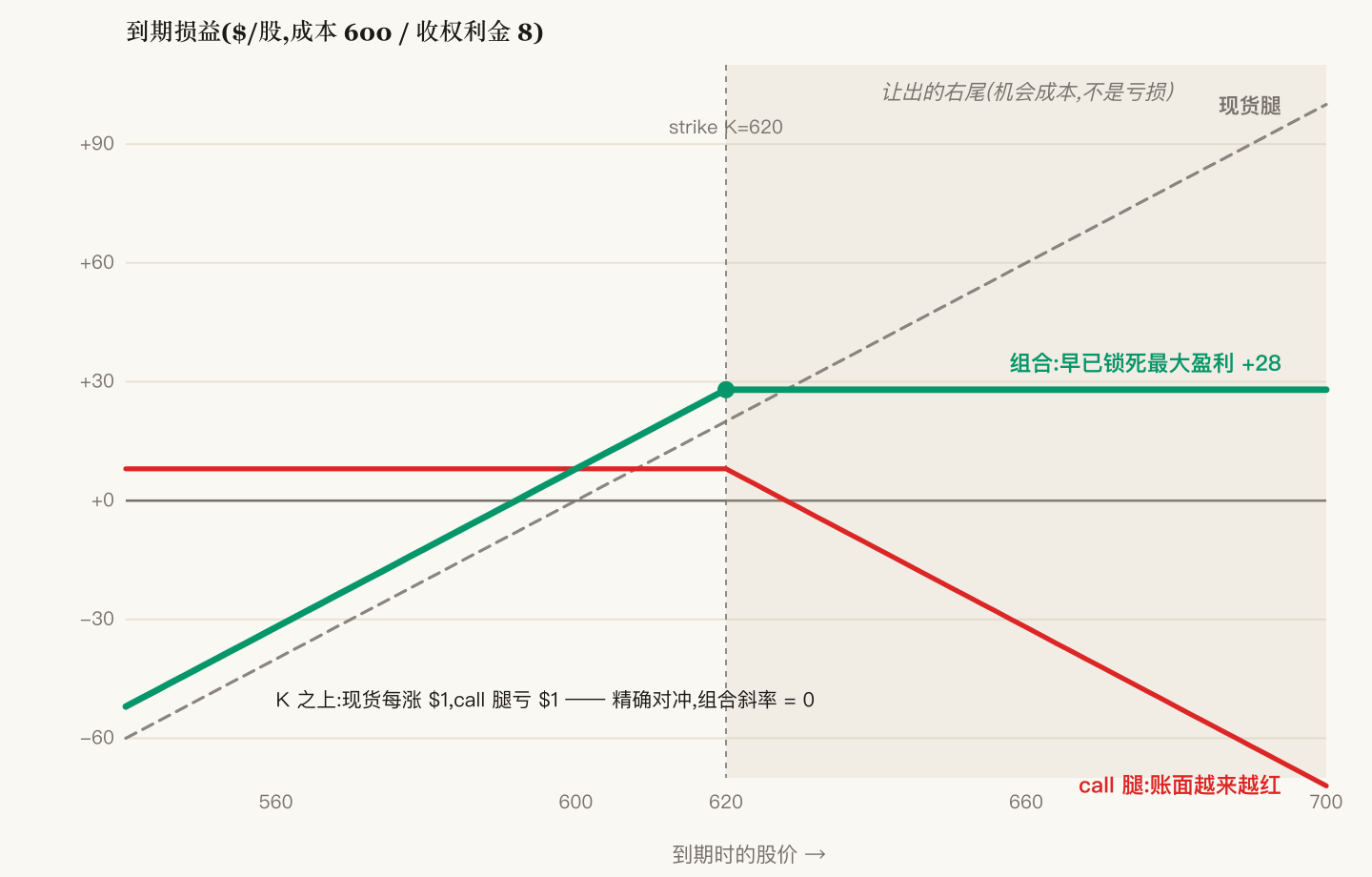

The principle fits in one sentence: the call leg's loss is not a real loss. Once the price crosses the strike, every 1 — a precise hedge. Your combined position locked in its maximum profit long ago. The red number is opportunity cost (the upside you sold away), not a loss. And "buying it back to stop the bleeding" converts zero-cost regret into realized cash losses — while re-opening unlimited exposure at the top.

The mechanics are easy. The hard part is me.

After the retreat I reconciled my trading log and found a pattern: every time I followed the rules I made money; every mid-session exception got punished. The rules had been right all along. Every loss was an execution failure.

So the final step was to revoke intraday-me's decision rights and replace them with three physical gates:

- No opening positions on red days — if the index is down more than 1% on the day, only closing/reducing orders are allowed. No new positions, including the seductive "premiums are so juicy after the drop."

- Leverage flag veto — run the leverage check before any order; above the line, only risk-reducing orders pass.

- Fixed trading window — hands move only on designated roll days; on all other days, watch only the distance to liquidation, never the P&L.

The rules were written by the calm after-hours version of me, precisely so that the feverish intraday version never has to make a judgment call.

Closing

The retreat deleted: single-name VRP stock-picking, automated trading, long volatility, index alpha, and the very idea that "options are an income source." What remains: a growth-beta core, a leverage cap that was computed rather than felt, defined-risk structures, and a few mechanical rules that keep emotion outside the door.

It sounds like retreating from a "sophisticated strategy" back to "naive holding." But what real money taught me is precisely this: the sophistication was a hallucination I was paying for; the naivety is the only edge a retail investor truly owns.