A Meat-Grinder Week for Chips — and My First Time in the Audience

Friday, July 10, 2026. SK Hynix rang the Nasdaq bell: a $26.5 billion raise, the largest US listing by a foreign company ever — bigger than Alibaba's 2014 debut — and the ADRs popped 15% on day one. On the other side of the same week, Intel slid roughly 20% from its high, in a selloff lit by Samsung's "record profit, circuit-breaker crash" earnings and fed by a process-yield delay and AMD taking the data-center crown.

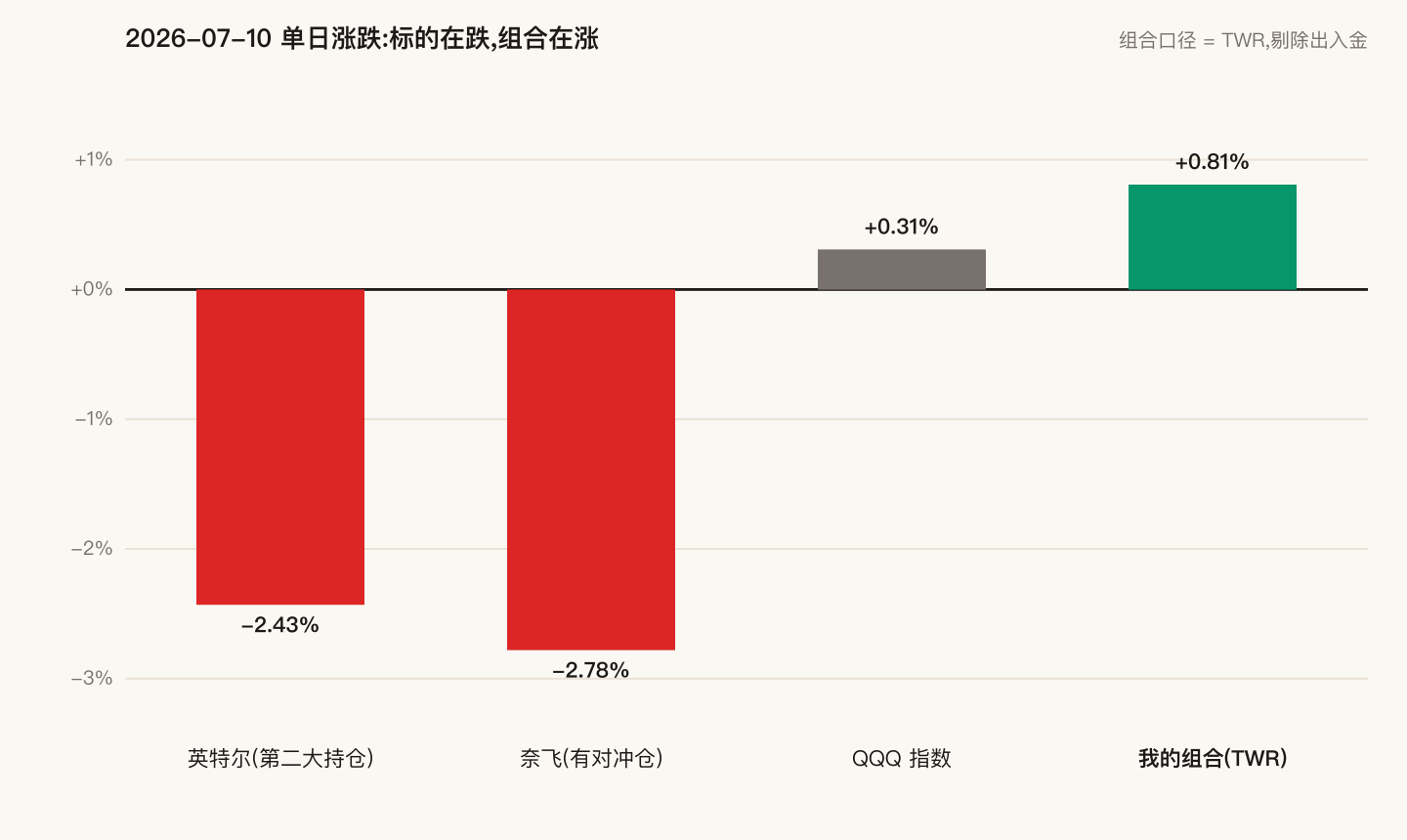

At the end of my last post I planted a flag: next time the meat grinder starts up, I want to be sitting in the audience. This week was probably the first time I actually was — my second-largest holding fell 2.4% on the day and 21% on the week, while my account finished the day up 0.8%, ahead of the index. This post is about why that steadiness was structural, not psychological.

1. The tape: ice and fire on the same day

The Hynix deal says a lot: AI memory is the year's most crowded story, and even after a week-long semiconductor rout the market swallowed $26.5 billion of fresh supply and still sent it up 15%. The money isn't gone — it's being choosy.

Intel's decline, meanwhile, wasn't panic; it was repricing. The advanced-node yield timeline slipped and the data-center throne changed hands — two pillars of the old story loosening at once. Same supply chain: a new king rings the bell while the old king bleeds, on the same trading day.

And the index? QQQ finished up 0.3%, still near record highs. The calm at the surface was held up by megacaps; underneath, semiconductors were violently changing hands. If you only watched the index, nothing happened this week. If you held a single chip stock, you lived through a miniature crash.

2. My day: 28 calls expired and the account slimmed itself down

My statement looks busy: 28 short calls expired — 27 were assigned, with two blocks of stock called away at prices agreed weeks ago; the last one expired worthless by a margin of 0.2%, premium fully banked.

But I made exactly one active move all day: inside my fixed trading window, I redeployed the freed-up cash into two rounds of covered-call re-builds, by the usual rules. The second order went in during the last pre-close window — the time the rules prescribe, not earlier, not later.

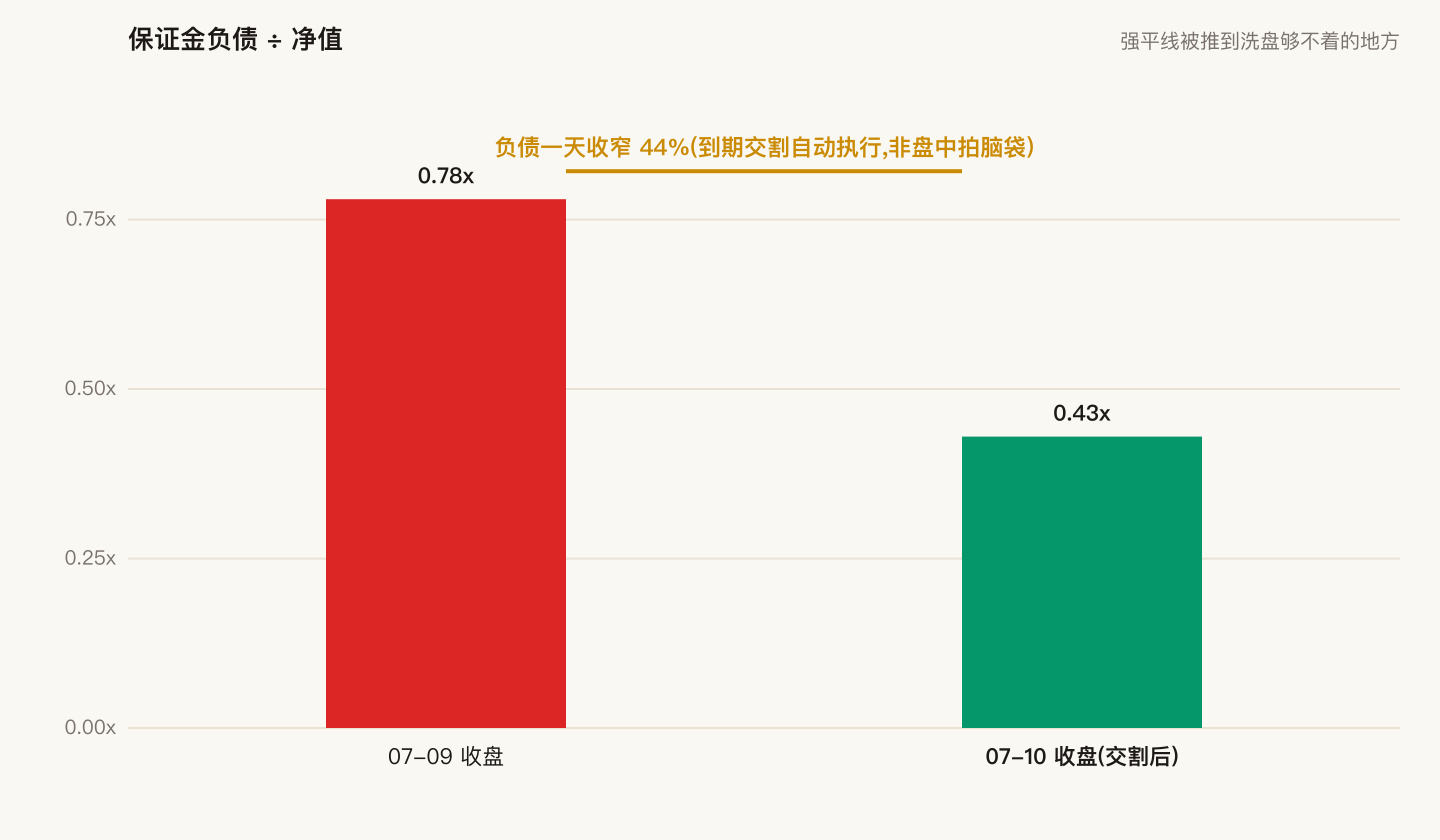

The result was a passive slim-down: margin debt shrank 44% in one day; debt-to-equity fell from 0.78x to 0.43x. No agonizing over "selling too early," no "maybe wait a bit longer" — assignment is a conditional event. When the condition arrives, it executes itself. The script was written two days earlier when I rolled; today I just watched it run.

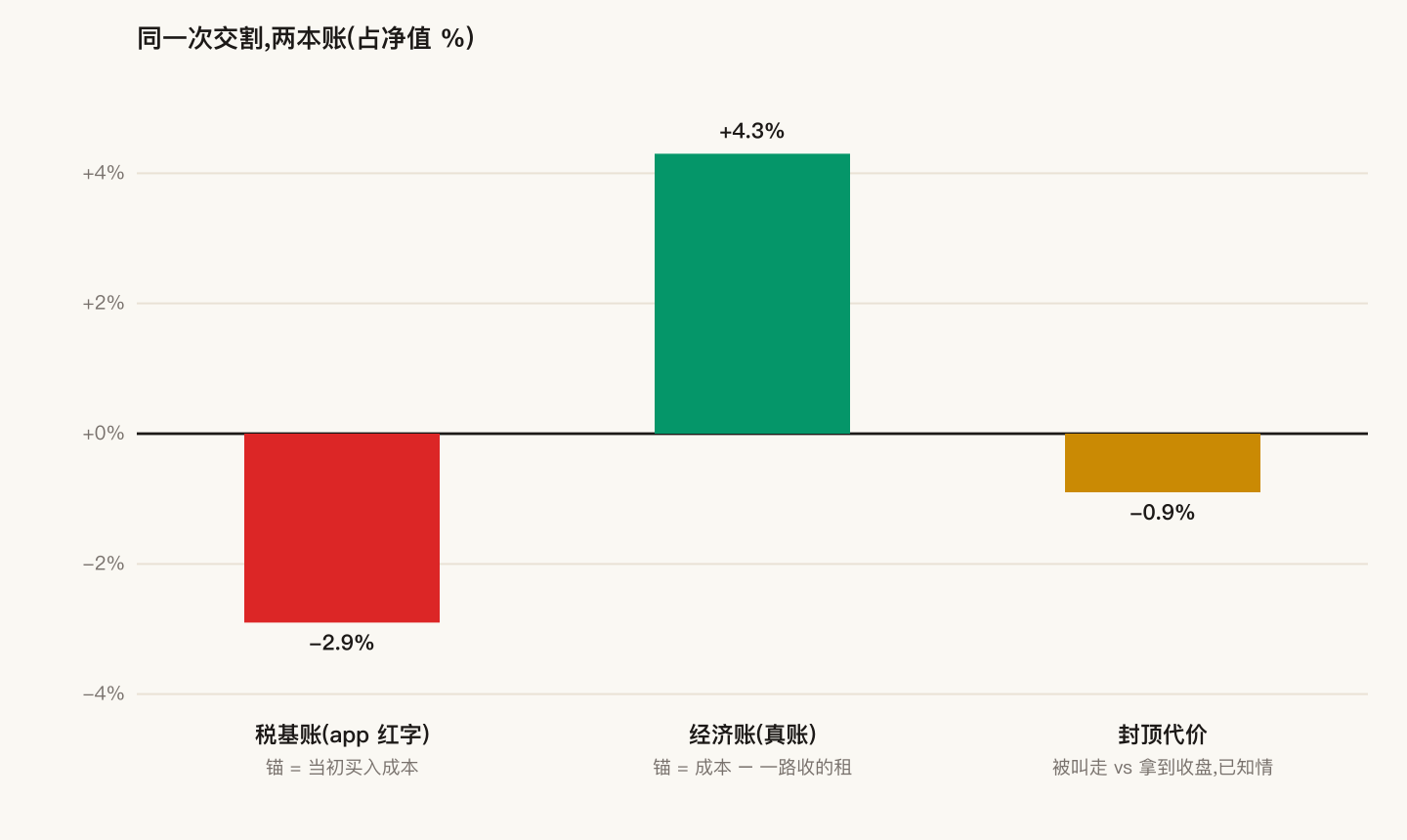

3. Two ledgers: the app shows red, the real book is green

The broker app printed an ugly red number today: the shares that got called away were old, high-cost lots, and against their purchase price this settlement "locked in" a loss of about 2.9% of net worth.

That's an anchoring illusion. These positions have been selling calls and collecting rent since they were opened, and the accumulated premium had long since pushed the effective cost down — about 9% lower on one name, about 25% on the other. Measured economically (settlement price versus effective cost), the same settlement was a positive 4.3% of net worth.

One settlement, two ledgers, one red and one green. The only difference is where the cost anchor sits: the app anchors on "what I originally paid"; the economic ledger anchors on "what the position has paid me back along the way." Judging a continuously-operated position by the app's red and green is like judging a rental property by a single month's mortgage bill.

And the honest footnote: because the index rallied hard these two days, the called-away shares would have earned roughly another 0.9% of net worth had I held them to today's close. That's the built-in cost of selling calls — capped upside — and I knew it the moment I sold. The rent and the cap are two faces of one contract; if you'll only acknowledge one of them, you don't deserve the rent.

4. Why it was steady: the structure was calm, not me

A heavy holding fell 2.4% in a day and 21% in a week. Six months ago I would probably have panic-sold into it at least once. This time there was no pain at all, for boring reasons:

- The falling shares were covered by deep in-the-money calls. For every dollar the stock dropped, the short call earned almost exactly a dollar back — the combination is nearly immune to downside (at the cost of being nearly immune to upside; see the 0.9% above).

- After settlement, the account's net directional exposure is only about 0.5x net worth. (Honest caveat: that's a point-in-time reading. A call-selling book gets longer on its own as the market falls; don't treat the number as a constant.)

I wrote last time that the grinder can only reach three kinds of people: the leveraged with a liquidation line, those who sell because it hurts, and those who watch the tape with itchy hands. I'm not fully desensitized — the debt is still there — but the liquidation line has been pushed beyond any shakeout's reach, the pain has no execution channel, and every action is locked inside a fixed window.

My mindset didn't get stronger. My positions just stopped handing it a knife.

5. The same three gates

Converging on the same place as the last two posts (not a coincidence — every road leads here):

- No opening trades on red days — big index down-days are for closing and reducing only;

- The leverage flag has veto power — past the line, only de-risking orders are allowed;

- A fixed trading window — act only at the scheduled time; intraday-me has no authority.

Every trade this week happened inside the window; every expiry ran a script written two days in advance. Next time a circuit-breaker kind of day arrives, I hope I'm still sitting right here. The audience seat isn't passivity — it's moving every moment that requires a decision to before the market opens.

Sources: Bloomberg — SK Hynix ADR debut · CNBC — Hynix's US listing plan · Yahoo Finance — record ADR offering · The Motley Fool — Intel's 21% week · 24/7 Wall St — Samsung earnings trigger chip selloff