WRITING

A One-Cent Roll That Paid Off Half My Debt: Assigning Myself on Purpose

July 15, 2026, Wednesday. Day three of the meat grinder: the same chip stock went −6.1% Monday, +4.5% Tuesday, and −4.4% again Wednesday — a morning analyst note warning its server-CPU share would nearly halve took back the whole rebound. The index drifted slightly lower, dragged by semis.

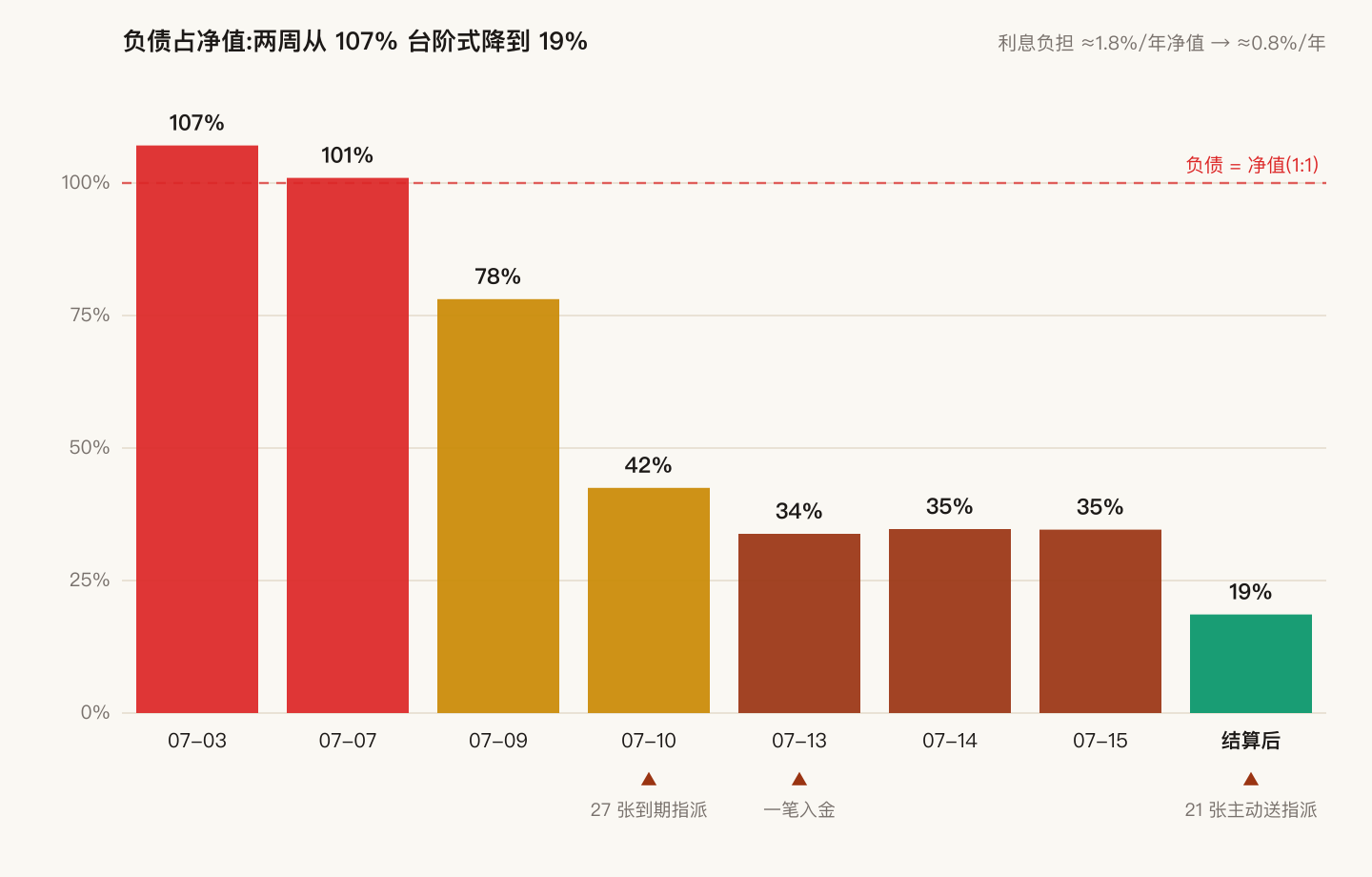

I did one thing that mattered today: I swapped 21 covered calls expiring Friday into same-day expiry at a lower strike, for a net credit of one cent per share. What did I buy with that? Tonight the clearinghouse will sell those shares for me at the strike — no sell order, no bid-ask spread, no commission, no market impact. One nearly profitless order cut my account's debt almost in half. This post is about turning "getting assigned" from an accident you dodge into a deleveraging tool you aim.

1. The tape: day three, the give-back

Last post covered the CPI-cooling chip rebound — Intel +4.5%, reclaiming lost ground. The script lasted exactly one day: Wednesday an analyst report warned its server-CPU market share would fall from 41% to 24%, stacked on cash-flow questions about the $5.7B Ireland expansion, and the stock gave back −4.4%. Three days: crash, rebound, give-back — one full round trip.

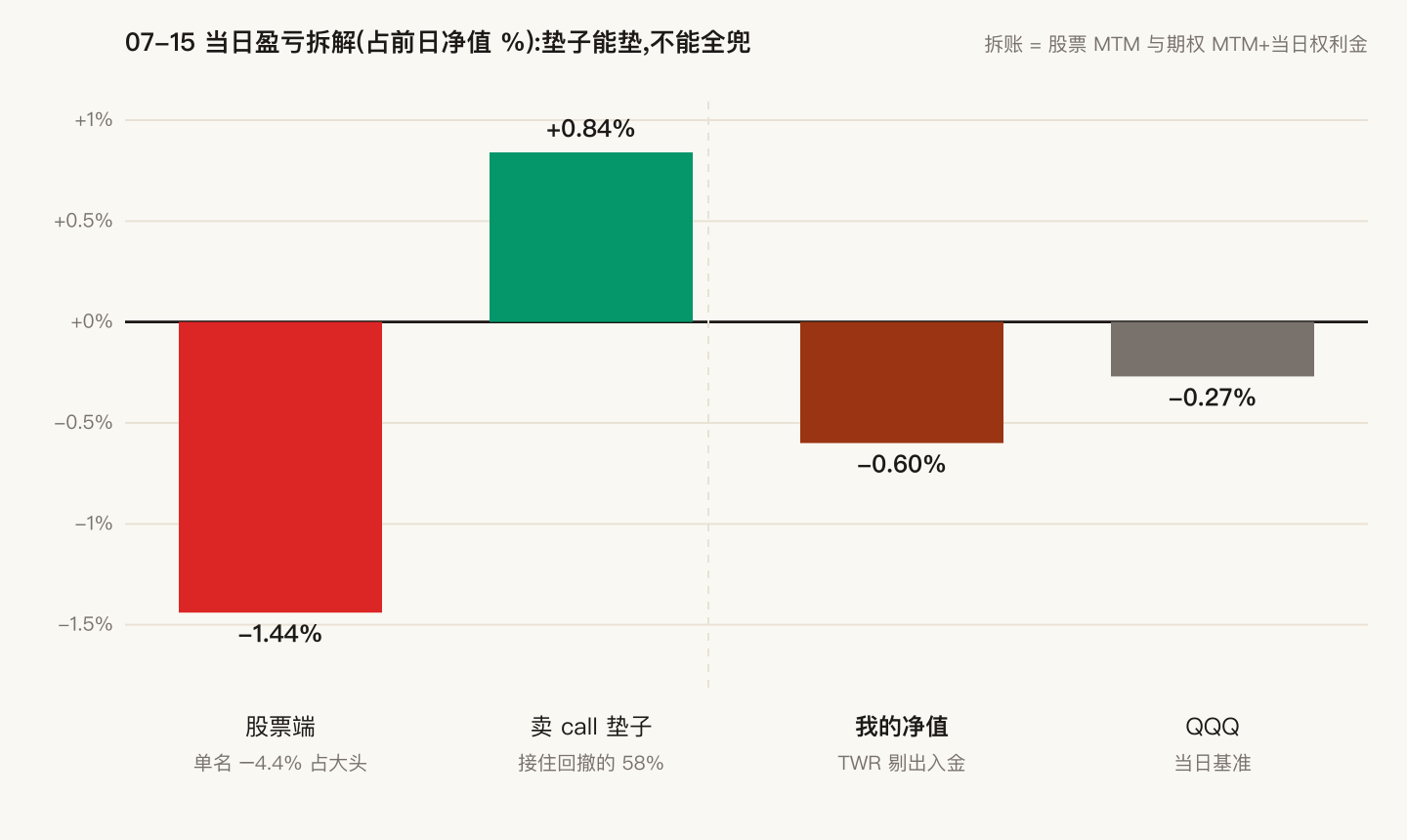

My portfolio finished the day at −0.60% versus the index's −0.27% — the scoreboard's first losing day since it opened, underperforming by 0.33 points. Where the money went:

Almost all of the underperformance is tuition paid for single-name concentration: one stock at 26% of net value, down −4.4% on the day. No cushion fully absorbs that. Which is exactly why today's protagonist had to show up.

2. The main event: using assignment on purpose

A covered call's natural ending has always been assignment: the stock finishes above the strike at expiry and gets "called away" at the strike price. Most tutorials teach you to dodge it — roll out, roll up, close early. Today I ran at it.

When the stock fell back near the strike zone in the morning, I placed one roll order with two legs:

- Buy back the Friday 105 calls — the stock was below 105, so everything I paid was time value;

- Sell the same-day-expiry 100 calls — the stock was above 100, so what I collected was intrinsic value plus a sliver of remaining time value.

Netted out: one cent per share, collected. That cent isn't profit — it's a price: what it bought me was moving Friday's settlement to tonight. The stock closed at 103, safely above 100, assignment confirmed — tonight the clearinghouse sweeps the shares away at 100 and cash lands.

Why this channel deserves its own post: dumping two thousand one hundred shares outright means facing three frictions — the bid-ask spread (your sell fills at the bid), market impact (you press the tape down yourself), and the timing anxiety of whether to split the order. Assignment is the clearinghouse's batch job: settlement at the strike, whole numbers, no spread, no impact, and option assignment carries no commission. For the same de-risking, this is the cheapest exit I know. Deep in-the-money calls quote pinned to intrinsic value, so the roll order itself leaks almost nothing — today's total friction was the half-cent of residual value inside that one cent.

One more ledger to lay open, because tomorrow the broker app will show me a row of red: these shares' tax basis sits around 111, and handing them over at 100 prints −10% on the statement. But two and a half months of rolling rent on this name has ground the effective cost down to about 71 — in economic terms, shipping at 100 is a +40% gross gain. Two ledgers, side by side, never blended: the one you look at decides whether you sleep tonight; the one you record decides whether you'll dare do this again.

3. Why this stock, why now

Not inspiration — a pre-written plan. This name was 26% of net value against my 20% single-name limit, and the remediation was written days ago: cure the breach via expiry assignment. The original plan settled Friday; today the stock dipped back into the strike zone, and moving settlement up to tonight cost one cent. Buy.

Two days early buys two fewer nights of gap risk: this stock demonstrated what ±5% daily moves look like just this week, and Friday is already the account's busiest expiry day (35 index calls await their own verdict). Hand in one exam early; the syllabus gets one page shorter.

Zoom out to the month and this is the third step down the same staircase:

The price tag, stated plainly: every step down was paid for with capped upside. The index has bounced these two weeks, and my cap costs sit line by line in the settlement ledger — not hidden. Insurance sellers collect premiums and pay claims. That is the entire business.

4. The cut I didn't make

The same morning I also queued the identical trade on the index: 13 Friday calls rolled into same-day expiry below the market — same assignment play. It sat for half an hour. I cancelled it.

The respectable intraday reason: the chip-stock cut had disciplinary authorization (limit breach plus a written plan); the index cut had none — it doesn't breach anything, so cutting it would be improvised market timing. The honest post-close review adds the other half: I couldn't let it go. The index is the core position, and settling at 715 means shipping below the 718 market. My hand hovered over the button and came back.

Both reasons are true. Cancelling was correct, but I'm writing this into the manual: the correct reason must be "this cut isn't in the plan," never "I couldn't part with it." Cuts that are in the plan allow no hesitation; cuts that aren't allow no itch. Only both sentences together close the loop that keeps emotion out of the trades.

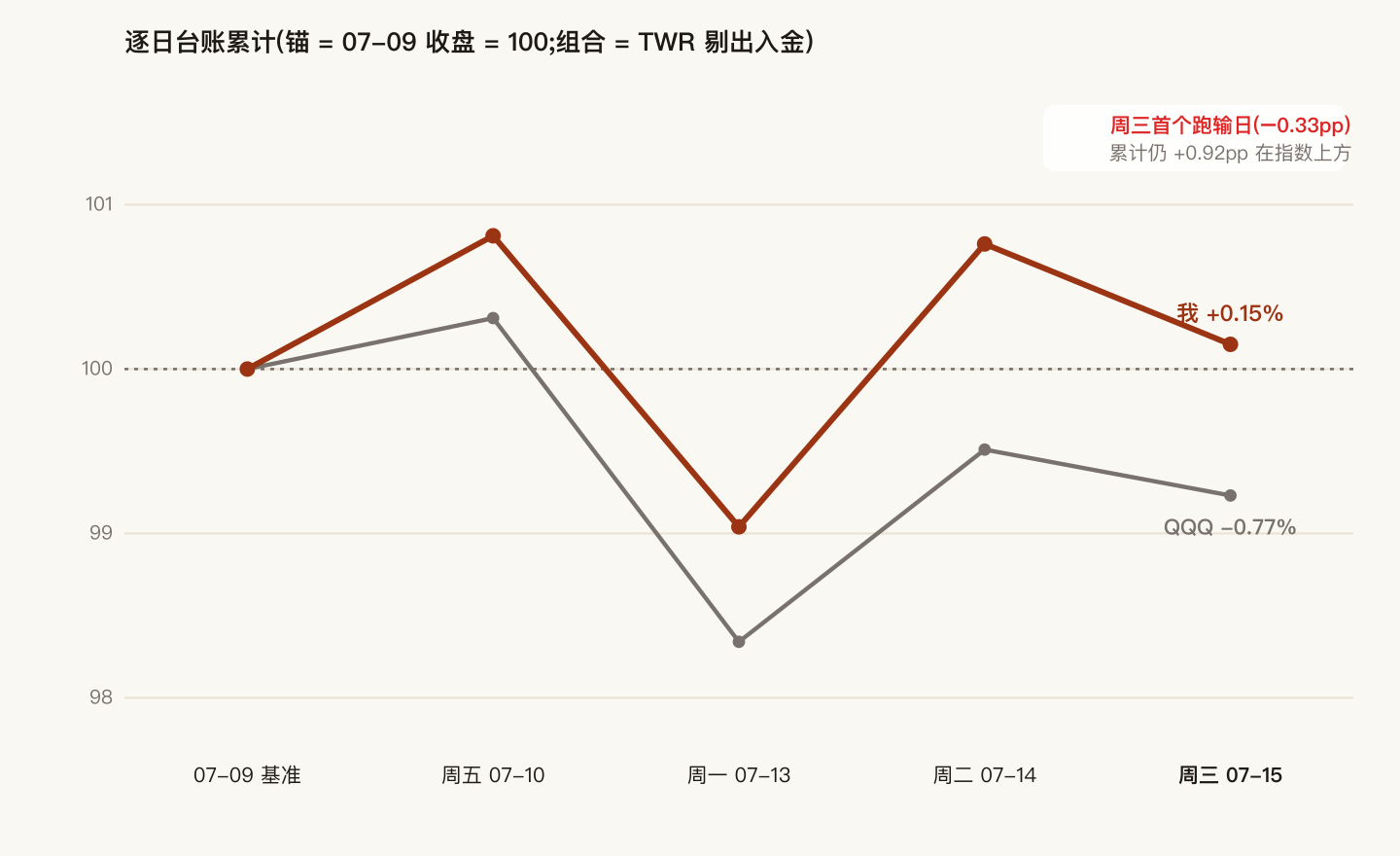

5. Scoreboard: first losing day

The daily ledger continues (anchor = Thursday-before-last's close = 100; portfolio in TWR, deposits excluded):

| Session | Tape | My portfolio | QQQ | Excess |

|---|---|---|---|---|

| Fri 07-10 | chip grinder | +0.81% | +0.31% | +0.50pp |

| Mon 07-13 | more selling | −1.76% | −1.90% | +0.15pp |

| Tue 07-14 | CPI rebound | +1.74% | +1.12% | +0.63pp |

| Wed 07-15 | give-back | −0.60% | −0.27% | −0.33pp |

| 4-day cumulative | whipsaw | +0.15% | −0.77% | +0.92pp |

No excuses for the first loss: the 0.33-point underperformance is almost entirely the 26% single-name concentration — the cushion caught 58%, and the remaining 42% is what holding a single name costs. Which is exactly why it gets cut to 9% tonight: the most useful thing a loss hands you isn't a lesson — it's the specific row of the position table that needs to change.

Friday's big exam is two days out. The syllabus is one page shorter; the remaining verdicts (35 index calls: settle, roll, or expire) will be made by Thursday — on Friday itself, I'll be in the audience again.

Last post said leverage breathes on its own: inhaling on the way down, exhaling on the way up. This post is the other half of the truth — the breathing machine manages the shape of your exposure, not the size of your debt. The size you cut yourself, and the best way to cut it is to let the clearinghouse do the cutting for you.

Sources: MarketBeat — Intel down 4.4% Wednesday · TradingKey — BofA warns Intel server-CPU share falling from 41% to 24% · Yahoo Finance — semis drag indexes lower (July 15, 2026 close)