The Meat Grinder Reversed — and My Leverage Breathed on Its Own

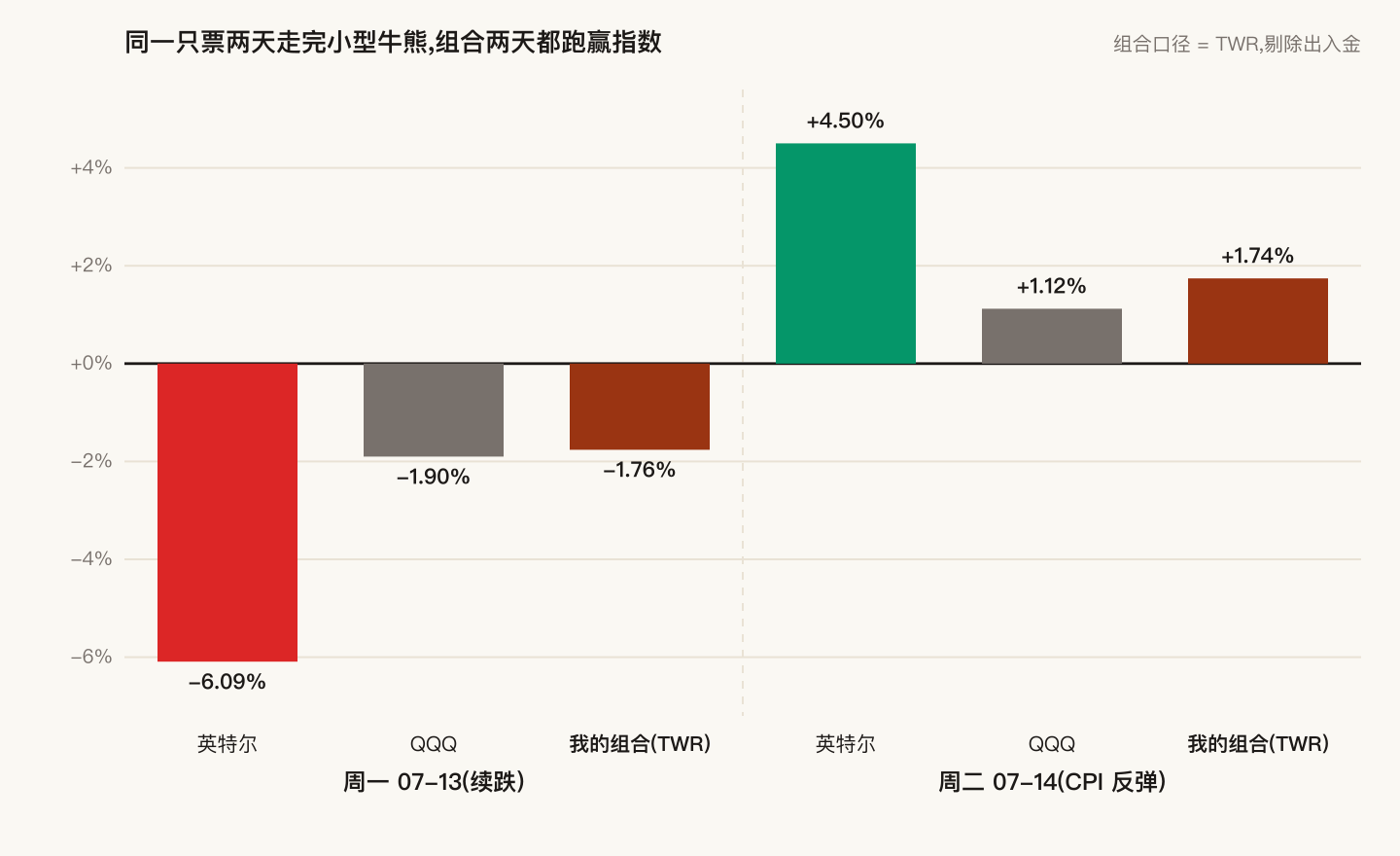

Tuesday, July 14, 2026. June CPI came in far below expectations — core inflation nearly flat month-over-month, headline prices posting their largest monthly decline in over six years. Rate expectations loosened, and yesterday's bleeding chip stocks rallied as a group: the Philadelphia semis ETF +2.5%, AMD +5%, Intel +4.5%, Nasdaq +0.9%. The same stock: −6% on Monday, +4.5% on Tuesday. A miniature bull-and-bear cycle in two sessions.

I did one small thing each day: Monday, into the decline, I closed two iron condors that had earned most of their premium; Tuesday, into the rally, I added one buy-write pair. The result: I beat the index on the down day and beat it again on the up day. This post is about the machine behind that — not that I predicted the reversal, but that a short-call book's negative gamma breathes for you: exposure grows into declines and shrinks into rallies. And what the breathing machine charges.

1. The Tape: The Grinder Changed Direction

Last post covered the semiconductor meat-grinder week — Intel down about twenty percent in a week. On Tuesday the script flipped: one cool inflation print put the rate-cut narrative back on the table, and the hardest-hit sector bounced hardest. Intel had its own headline too — a $5.7 billion expansion of its Ireland fab — and closed back above 107.

The interesting part isn't the bounce; it's the rhythm: Monday −6%, Tuesday +4.5%. If the pain made you sell Monday night, you turned a two-day round trip into a one-way ticket — on board for the entire descent, on the platform for the climb.

I didn't sell on Monday. Not because I'm tough — because the pain couldn't reach me: the falling positions were covered by in-the-money calls, and for every dollar the stock lost, the call side clawed almost a dollar back. Last post explained that structure; this week it took another shift on duty.

2. My Two Days: Harvest on the Down Day, Plant on the Up Day

Monday (down day): harvest. Two QQQ iron condors placed about a month ago had already earned 89% and 81% of their maximum premium. The residual tail was worth a dozen percent — and collecting it meant standing three or four more days of expiry risk. Volatility spiked on the down day, which made the buyback cheaper, so I closed both inside my fixed trading window and banked the profit. I also rolled a same-day-expiry call out by two days.

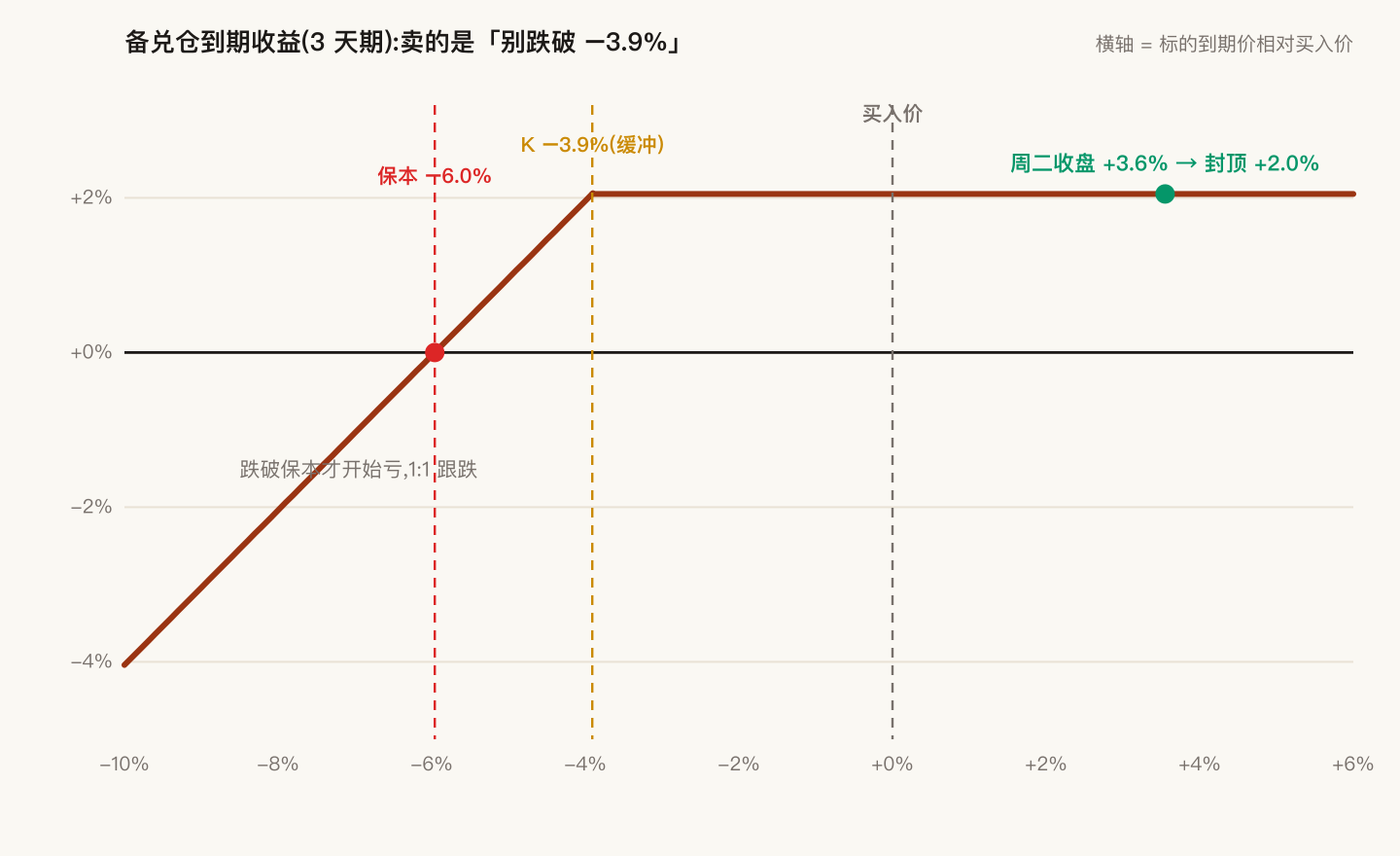

Tuesday (up day): plant. In the morning window I added one buy-write pair: bought stock and simultaneously sold a three-day in-the-money call struck 3.9% below my purchase price. The meaning of that combination: I'm not betting on more upside — any rally is capped at +2.0%; I only need the stock to not fall more than 3.9% in three days to collect that 2.0%; actual losses don't start until −6.0%. The payoff structure was locked the moment I bought. Nothing about the next three days requires a decision from me.

The two days had one thing in common: neither trade was a reaction to the market; both were executions of a price. The condor exit line was set the day the trade went on (close at 80–90% of premium earned). The buy-write's three lines — cap, cushion, breakeven — were computed before the order. The market merely delivered prices to my levels.

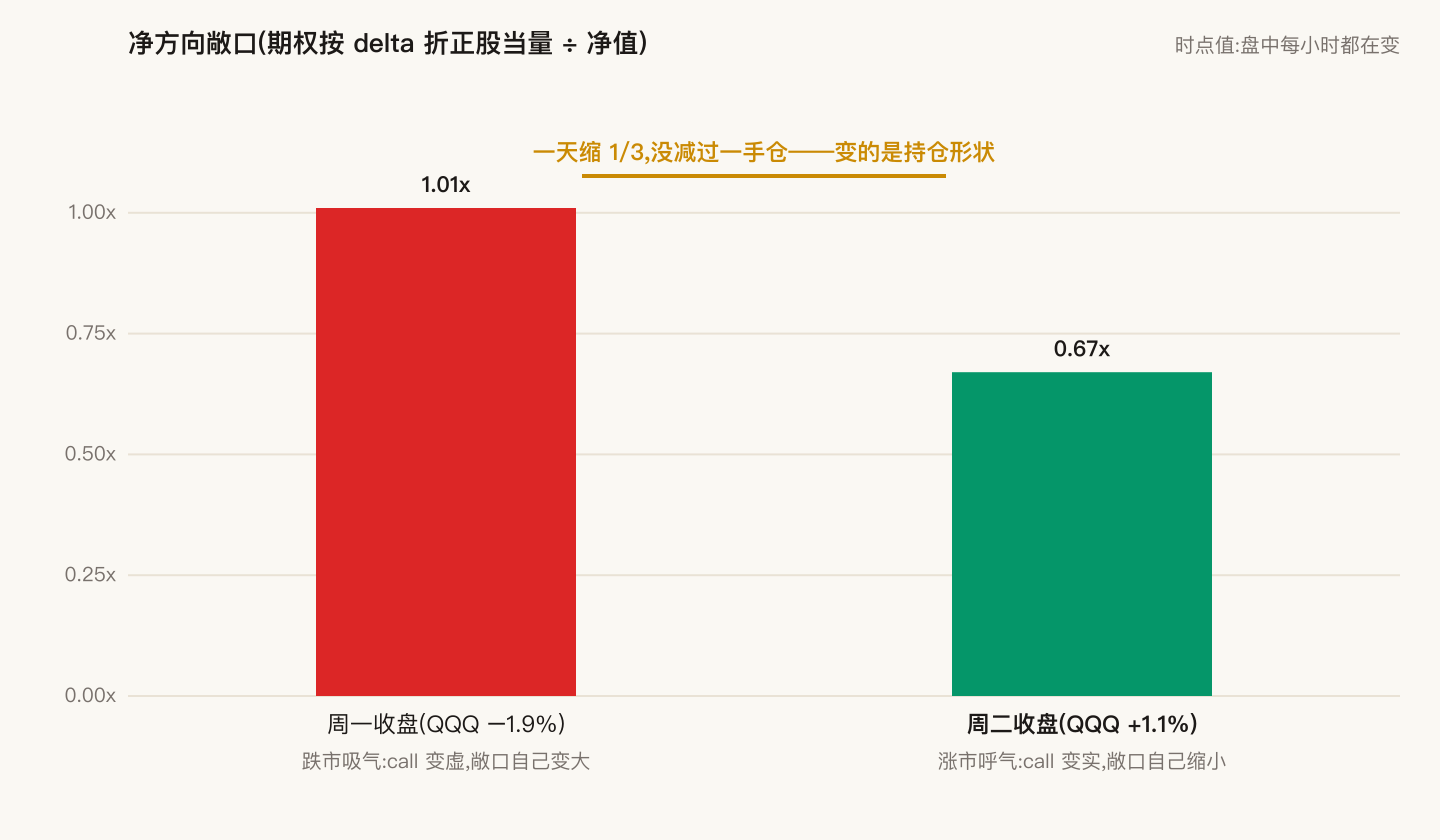

3. Leverage That Breathes: Longer into Declines, Shorter into Rallies

This is the part I actually want to write about. Watch my account's net directional exposure (all options delta-converted to stock equivalents, divided by net liquidation value):

- Monday close: 1.01×.

- Tuesday close: 0.67×.

Exposure shrank by a third in one day — and I didn't reduce a single position. What changed wasn't the holdings but their shape: when the underlying falls, short calls go out-of-the-money, their hedging force decays, and the book's net exposure automatically grows — the account gets longer into the decline, positioned to catch the rebound in full. When the underlying rallies, the calls go deeper in-the-money, the hedge stiffens, and net exposure automatically shrinks — the account gets shorter into the rally, locking profits progressively tighter.

That's the breathing: inhale on the way down (exposure grows), exhale on the way up (exposure shrinks). In a whipsaw like Monday-down-Tuesday-up, it lands on the right beat by construction — an automated buy-low-sell-high.

But there is no free breathing machine. The full ugly truth:

- This property's proper name is negative gamma, and in trending markets it gets hit from both sides. In a sustained crash, exposure grows as you fall and losses accelerate. In a sustained melt-up, exposure shrinks as you rise and gains are capped. The premium a seller collects is the insurance fee charged in advance for both of those one-way penalties. These two days felt good because the tape happened to be exactly the chop this structure loves; hand it a trending market and the same book looks bad.

- Exposure is a point-in-time reading, not a constant. 1.01 and 0.67 are photographs taken at two closes; intraday it moves every hour. Use it for risk control, not for pride.

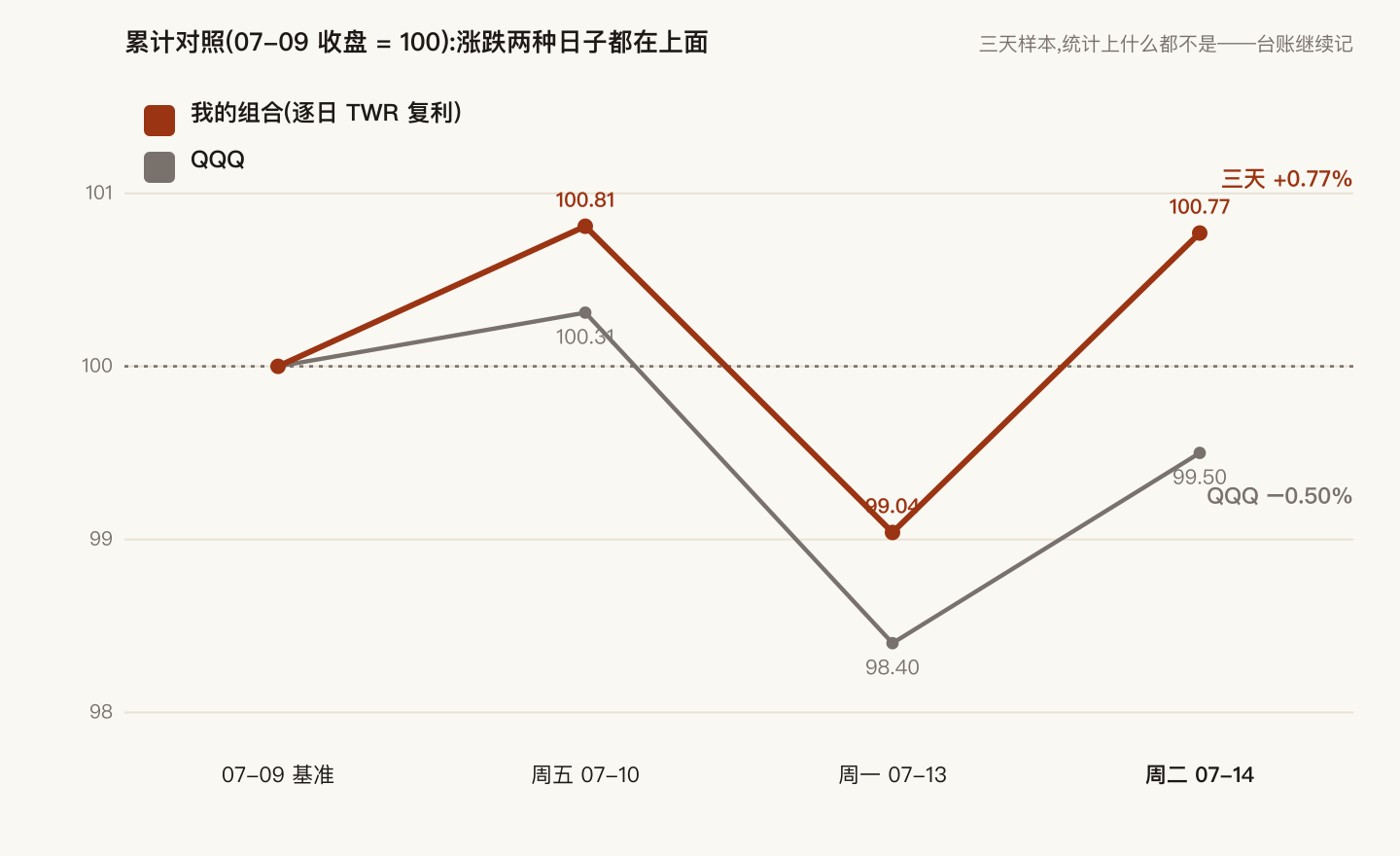

4. Scoreboard: Three Days Is Not a Sample

The daily ledger I started keeping last Friday (baseline = last Thursday's close = 100; portfolio measured as TWR, deposits excluded):

| Session | Tape | My portfolio | QQQ | Excess |

|---|---|---|---|---|

| Fri | chip grinder | +0.81% | +0.31% | +0.50pp |

| Mon | more selling | −1.76% | −1.90% | +0.15pp |

| Tue | CPI rebound | +1.74% | +1.12% | +0.63pp |

| 3-day total | whipsaw | +0.77% | −0.50% | +1.27pp |

Three for three — but let me write this line before the conclusion: three days is statistically nothing. This stretch (a sell-off followed by a bounce) is precisely the water a premium-selling structure swims best in. Give it a stretch of one-way melt-up and I will likely underperform for days in a row — that's when the cost of the cap gets smeared across my face daily. The ledger keeps recording; the sample will grow up on its own.

5. Friday Is the Big Exam

This Friday is a major expiration: most of the calls on my book expire that day, and this rebound is pushing them back in-the-money one by one. Either the stock gets delivered at the agreed prices (a script written weeks ago), or the calls get rolled to the next cycle to keep collecting rent — the decisions will be made by Thursday, and on Friday I'll be back in the audience.

Last post's flag was "next time the meat grinder starts, I want to be in the audience." This week I'll add one line: the audience seat isn't just for crashes — a rally isn't worth jumping out of your seat for either. Up and down belong to the market; breathing belongs to the structure. My job is reduced to keeping the ledger after each close.

Sources: 24/7 Wall St — cooling CPI sparks chip rebound, AMD +5%/Intel +4% · TheStreet — market close, July 14, 2026 · The Motley Fool — inflation cools to 3.5%, matching 2020 lows · FXLeaders — Intel's $5.7B Ireland expansion · CNBC — live market updates