Buy Behavioral Stubbornness with Structural Reversibility

"Nothing is more dangerous than an idea, when it is the only one you have."

This line is from the French philosopher Alain (Émile Chartier). I first read it in a discussion of software architecture — don't weld your system to a single solution. Later I realized it governs far more than software. It governs trading, marriage, partnerships, buying a house, and how I allocate my energy every single day.

This piece is my attempt to write the whole thing down once. It's made of three parts: the reversibility mindset that puts a price on taking things back, the ego calibration that's pinned to facts, and the solution to the language trap of "persistence versus stubbornness." Bolt the three parts together and, across trading, life, and engineering, they're the same algorithm.

I. Reversibility isn't "can you take it back" — it's "how much does taking it back cost"

First, correct a naive reading: sorting choices into two bins, "reversible" and "irreversible." The real world has almost no absolutely irreversible choices — even having a child is, literally, "reversible" (surrender custody). The real variable isn't whether you can, it's the friction cost of taking it back.

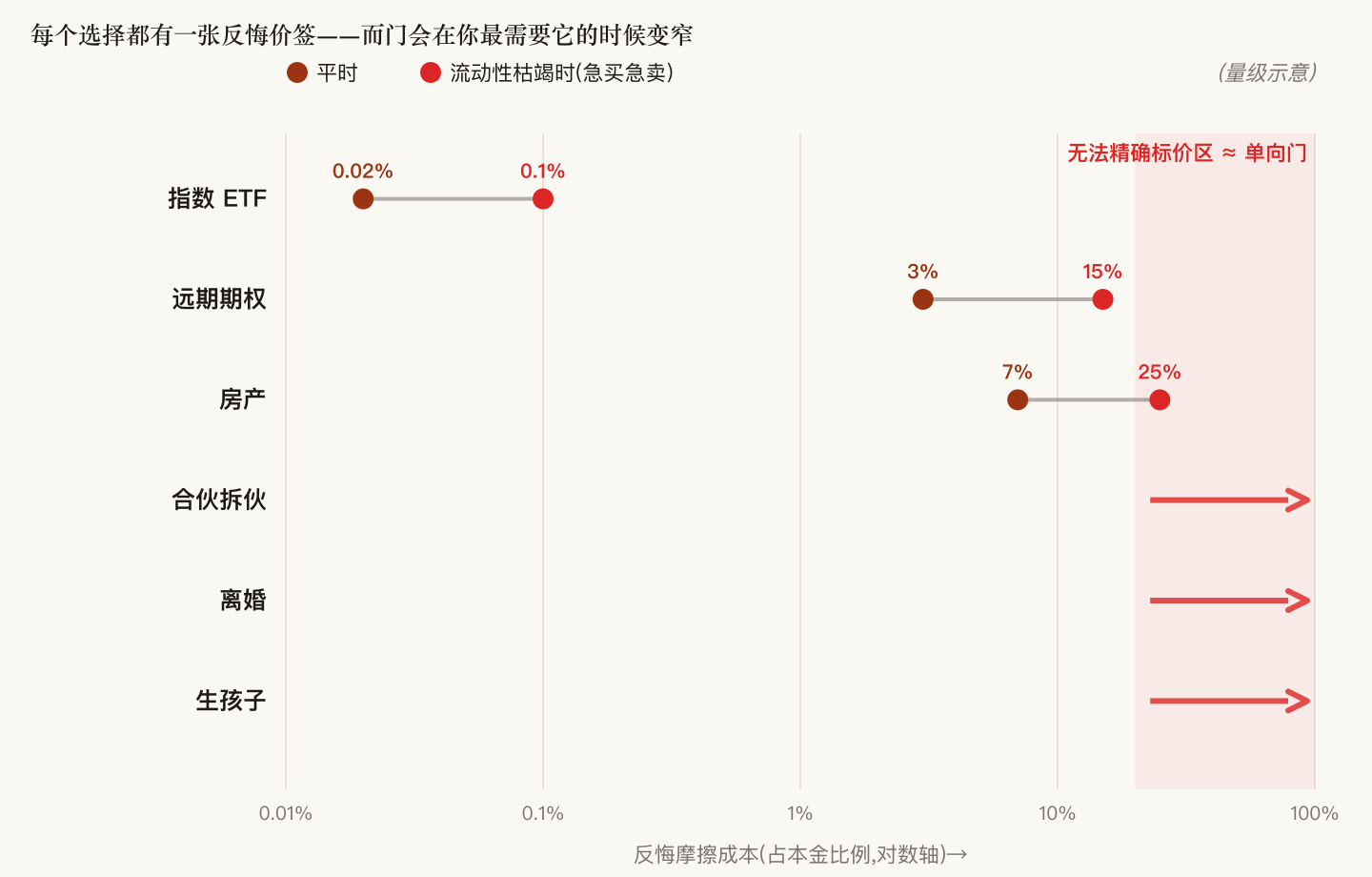

Financial markets have a ready-made measure for this: the bid-ask spread. The price you pay to buy something, and the price you can sell it back at when you change your mind — the gap between them is that choice's regret tax. This concept generalizes to every choice:

| Choice | How to take it back | Friction cost |

|---|---|---|

| Index ETF | Two clicks to sell | A few basis points, settles in seconds |

| Long-dated option | Close at a discount | Spread often a few percent; illiquid contracts, double digits |

| Real estate | List and sell | Agent fees + taxes + time; one round commonly 5–10% |

| Being a boss / project lead | Resign | Reputation + relationships + sunk time; hard to price precisely, but high |

| Starting a company with a friend | Split up | Interest disputes + the friendship itself; close in nature to divorce |

| Marriage | Divorce | Asset division + psychological cost + social cost |

| Having a child | Exists literally | Support costs + psychological + moral cost; so wide it's effectively a one-way door |

Two disciplines follow from this price-tag table:

First, before making a choice, put a price on "taking it back." Not "will I regret it" — no one can answer that — but "if I regret it, how much does exiting cost." Willing to pay that price? Then walk through the door. Can't afford it? Then don't buy on credit with "I definitely won't regret it." This is the single most actionable line in the whole philosophy.

Second, reversibility is state-dependent: the door narrows exactly when you need it most. Real estate normally trades at a 5–10% spread; when liquidity dries up, a forced sale might mean a 20–30% discount — everyone who has to buy or sell in a hurry loses, because the spread blows out at the worst moment for the market. A long-dated option can normally be closed; the instant panic hits, the spread is unwatchable. A partnership is "always negotiable" — until the day a real interest dispute erupts, when the negotiation cost detonates instantly. So when you price the regret, price it for the worst case, not for today's tape.

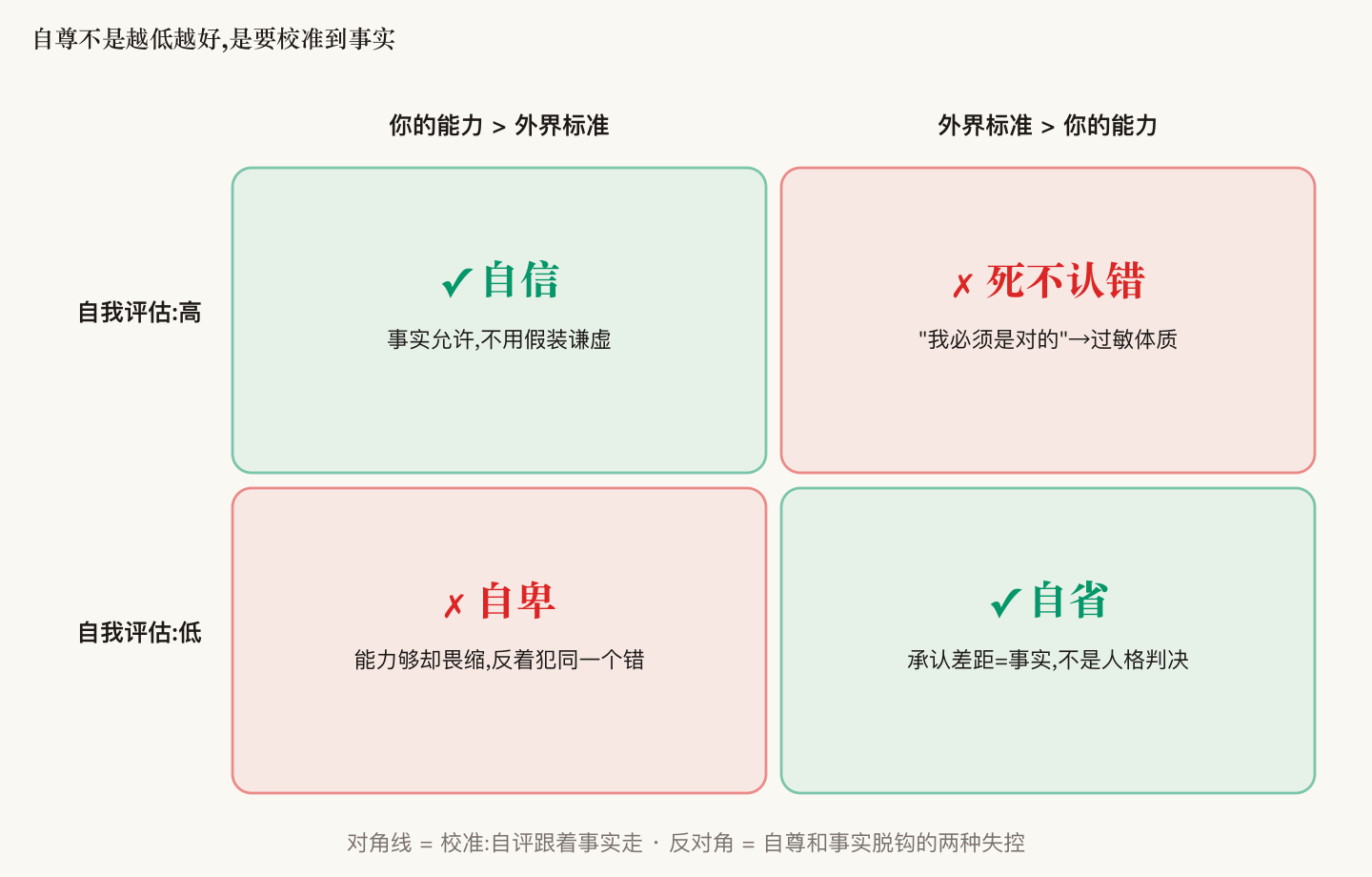

II. Ego isn't better the lower it goes — it should be calibrated

The last section governs choices; this one governs emotion — whether you can afford the admission tax.

Let's be fair first: ego has a function, called self-affirmation. A person has to believe in and respect themselves first, or their words carry no weight and no one gets influenced by them. Zero ego isn't equanimity, it's inferiority — a different kind of paralysis. So the question was never "how low should ego go," it's where ego is pinned.

The wrong way to pin it: pinned to an emotional need — "I must be right." The right way: pinned to objective fact. There are only two rules:

- The objective standard is well below your ability → be confident, of course, no need to fake modesty.

- The external standard is well above your ability → objectively admit you're not good enough right now. This is self-reflection, not inferiority — the gap is a fact, not a verdict on your character.

The picture makes it clear: what loses control was never "high ego," it's ego decoupled from fact. Doing badly yet insisting "I'm right," so every piece of negative information becomes a personal attack and every admission of error feels like cutting flesh; conversely, having enough ability yet cowering is the same error committed in reverse. The decoupled person has an allergic constitution — a single candlestick, a word of criticism, one dissenting opinion, and the whole body inflames, spending all day scratching. The calibrated person has a normal constitution: the same stimulus lands and is merely one data point for updating the assessment.

Calibration has one advanced move: switch the ego's anchor from "I'm right" to "I can correct." The former gets hurt every time you err; the latter gains value every time you correct. Make that switch and the admission tax drops straight to zero — your character was never staked on "being right this time," so there's nothing to attack.

III. Persistence or stubbornness? Before the result is in, language won't tell you the answer

Here hides a language trap. The very same behavior — persisting at one thing under pressure — if the result is good, everyone calls it "perseverance"; if the result is bad, the exact same thing gets renamed "stubbornness." The word is issued afterward based on the result, not beforehand based on the behavior. "Being driven" is the same: win and it's ambition, lose and it's overreach.

This means "I should persist" and "I should be flexible" are both empty beforehand — both wait on the result to be cashed out, and at the moment you decide you precisely don't have the result. Trying to use a maxim to decide whether to persist or turn around is asking language for something it can't give.

So what can you actually control beforehand? Only one thing: structure — cap the cost of "what if this time it's stubbornness" in advance.

| Layer | What it is | Should it be flexible |

|---|---|---|

| Structural layer | Position size, leverage, cash buffer, how you allocate energy and identity | Must be reversible — by the rule in Section I, only buy tickets whose regret tax you can afford |

| Belief layer | Directional judgment, long-term thesis, the core playbook validated over and over | Can be stubborn — someone who flips direction three times a year has no compounding |

Most people's configuration is exactly backwards: they turn around constantly at the belief layer (doubting the big direction daily) and weld a one-way door shut at the structural layer (maxing out leverage, keeping no cash, staking their whole identity on a single title).

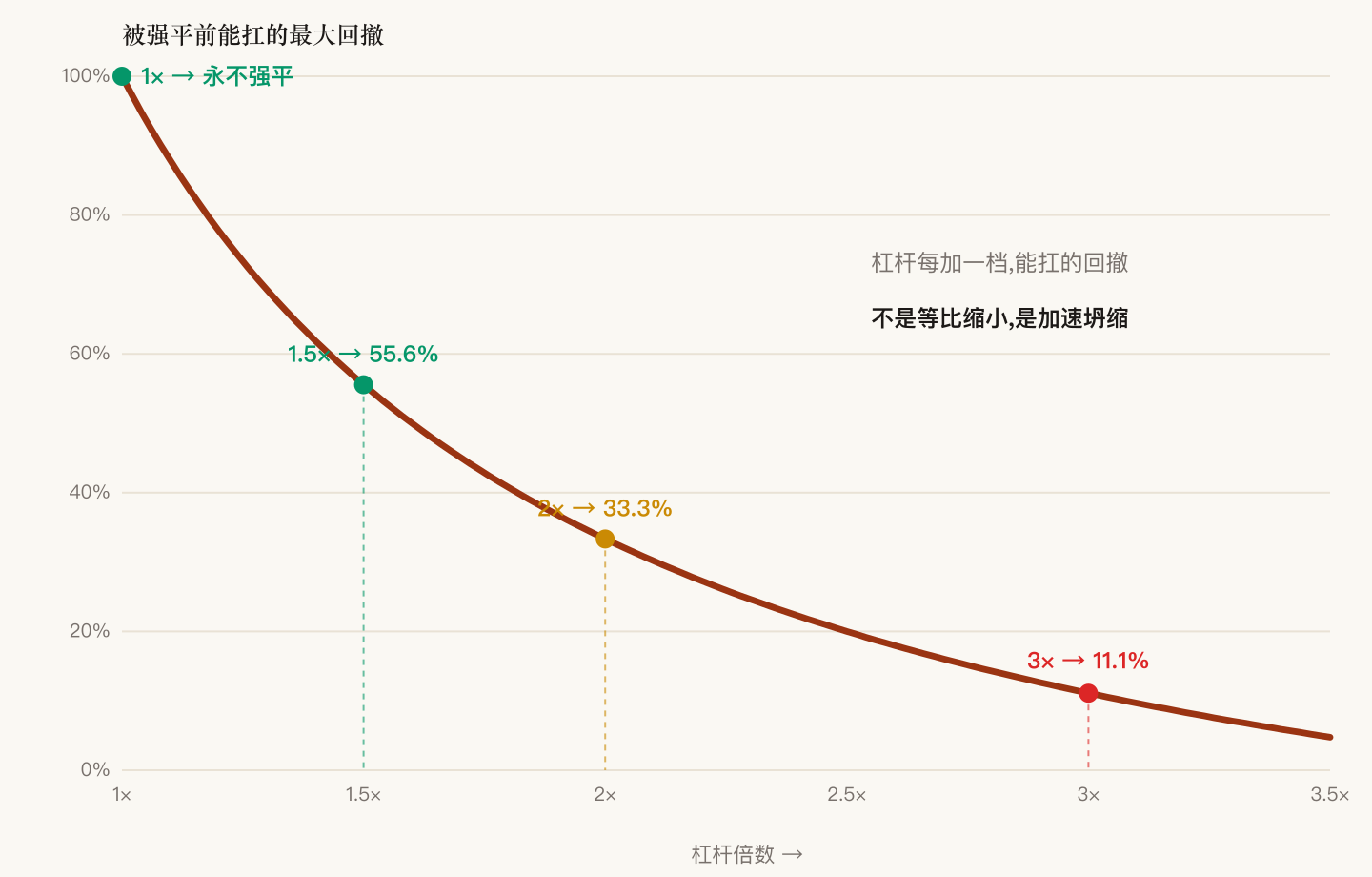

The most typical one-way door in the structural layer is leverage. Not because leverage amplifies volatility — that's just math — but because once leverage crosses a certain line, the market acquires the power to decide for you: forced liquidation, which always happens at the worst moment, and is irreversible. That line can be computed precisely (assume a maintenance margin of 25%):

At 1.5x leverage, you can withstand about a 56% drop before liquidation — a historic-scale crash might not even reach you, and whether to turn around remains your decision. At 2x, the buffer is only 33%; one decent bear market can touch it. At 3x, only 11% — a single week of bad tape can confiscate your steering wheel. Note this is exactly the extreme form of "the door narrows" from Section I: normally you feel you can trim anytime, but on those crash days it's the market trimming for you, at its price.

Once the cost is capped, you gain a luxury: you don't have to guess in advance whether history will issue you the "perseverance" or the "stubbornness" label — you can afford to live with either. I hold the index, sit still through crashes, don't time the market; that stubbornness isn't courage, it's that I paid for it in advance at the structural level. First guarantee you can afford to be wrong, and only then can you talk about holding the line.

IV. Life is isomorphic: stopping out of a relationship and stopping out of a position are the same move

Move the lens away from trading, and the same algorithm looks like this in life.

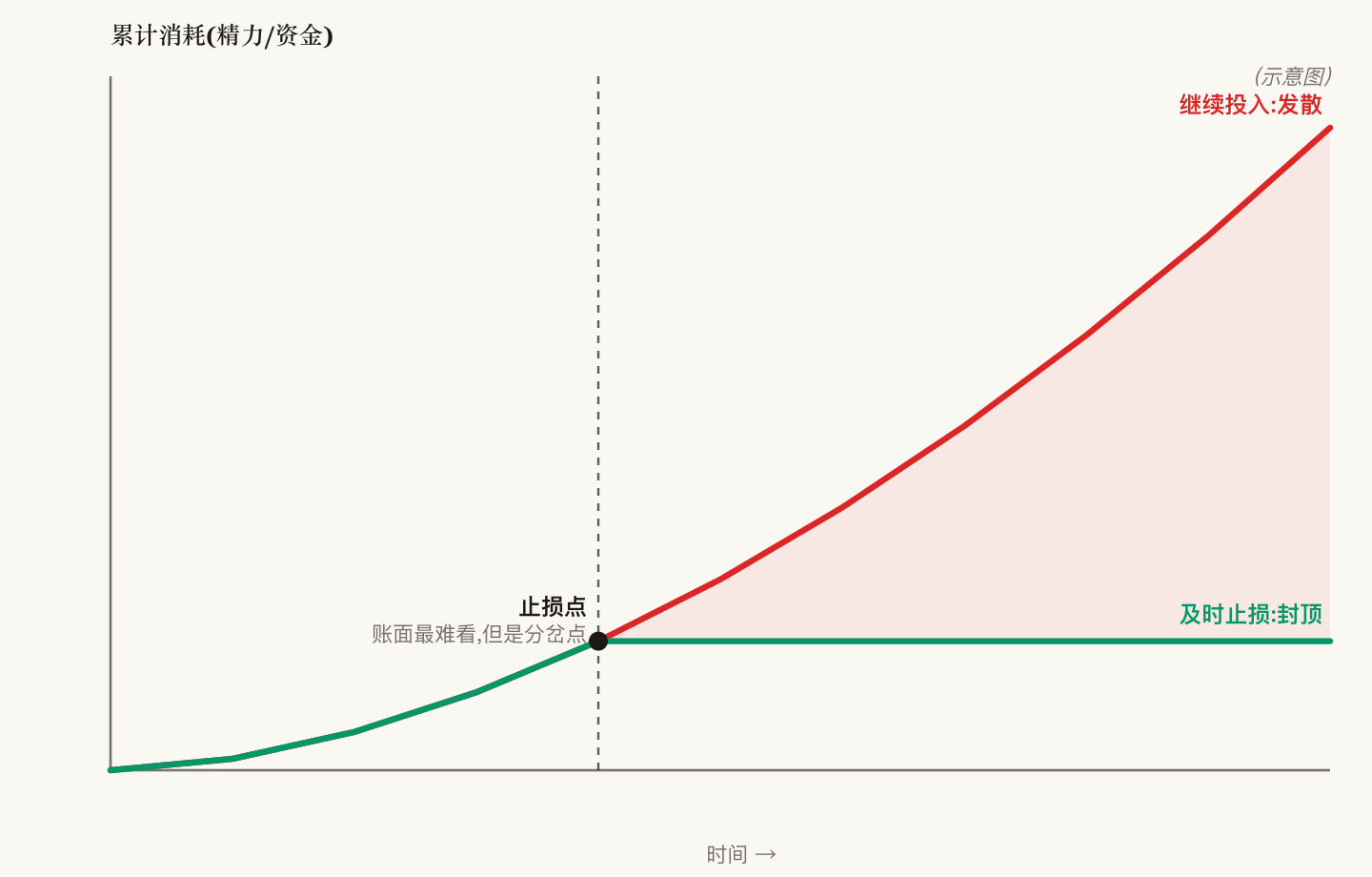

Some people, some things, drain your energy and money continuously. The textbook predicament: "I've already put in so many years, so much money, so much feeling — if I quit now, wasn't all of it wasted?"

This is the sunk-cost fallacy — its name in trading is averaging down a losing position. They're the same error: letting a cost already paid and unrecoverable decide where to go next. The correct algorithm has only one line: look only at the margin — from today on, what does each additional unit of energy invested expect to return? If it returns nothing, stop out, no matter how much has already sunk into the account.

What stands in front of the stop-loss is usually not reluctance to let go of the other person — it's reluctance to let go of the self-image of "I didn't misjudge back then" — the admission tax. This loops back to Section II: with the ego pinned to "I'm right," this tax is so expensive it makes people procrastinate for years; pinned to fact, misjudging a person, like misjudging a stock, is a normal probabilistic outcome, not a bankruptcy of character. Apologize, thank, exit, walk away — run the whole sequence, take your energy back, and put it where it can compound.

While we're at it, log the emotion into this ledger too: emotionality itself is a cost item. Those who are easily angered, who won't concede verbally, who win arguments by being cutting — they rarely accomplish much. Not because they're stupid, but because their bandwidth is entirely paid out to "defending the self-image," a project with zero return. An argument decides who wins; it doesn't change who's right, and it changes the product even less.

V. Engineering is isomorphic: good architecture is just making turning around cheap

People who write software should be most familiar with this philosophy, because modern software engineering is built almost entirely around "driving down the regret tax":

| Engineering practice | Essence |

|---|---|

| Modularity, loose coupling, interface abstraction | Let a local rewrite not implicate the whole — drives down the regret tax at the architecture layer |

| Short iteration cycles, fast feedback | Compress the latency of "discovering you were wrong" to the shortest — the earlier the error is found, the cheaper |

| Version control, one-click rollback | Every change keeps a way back — everything is a two-way door |

| Separation of concerns | Business logic not welded to the presentation layer — that's why a browser app can move to a mobile app at all |

Conversely, nearly every engineering disaster translates to "regret-tax bankruptcy": a single solution welded in with no Plan B, refactoring so expensive nobody dares touch it, a release that can't be rolled back. It's the same story as a blowup, and as a draining relationship that took five years to end — three dialects of one story.

VI. The same algorithm

Lay it out side by side and it's one table:

| Trading | Life | Engineering | |

|---|---|---|---|

| Before entering | Price the close-out (spread/liquidity) | Price the exit (the real cost of splitting up/divorce/surrendering custody) | Price the refactor (coupling) |

| Structural reversibility | Leave a leverage buffer, cap risk | Don't stake your whole net worth and identity on a single relationship or a single title | Loose coupling, rollback-able |

| Turn around when wrong | Stop out, don't average down | Terminate the drain, disregard sunk cost | Rewrite from scratch, don't guard bad code |

| Emotional cost of turning around | Ego calibration → admitting error is painless | Ego calibration → exiting is painless | Ego not bound to the old solution |

| Belief-layer stubbornness | Hold core positions long-term, through the crash | The long-term few things, unshaken for ten years | Core architectural principles don't sway with the wind |

Written as an algorithm, it's five steps:

- Before any choice, put a price on "taking it back," and price it for the worst liquidity case. Can't afford it, don't enter; can afford it, enter boldly.

- Cap the cost of being wrong at the structural level. Leverage, position size, identity, energy — none may take a configuration where "one mistake and you're out."

- Calibrate ego to fact. Standard below ability, be confident; above ability, reflect. Switch the anchor from "I'm right" to "I can correct," and the admission tax goes to zero.

- When wrong, turn around immediately; look only at the margin, disregard the sunk.

- On the validated few beliefs, compound stubbornly. Perseverance or stubbornness — let history issue the label; you're only responsible for living to the day it's issued.

The disappearance of internal friction is only a byproduct. When "I was wrong" no longer triggers pain, when the cost of every mistake is capped in advance, anxiety loses its object — the essence of anxiety is standing guard at a one-way door you welded shut yourself.

Buy behavioral stubbornness with structural reversibility. That's everything that line taught me.