WRITING

Catching the Knife at 708 with a Floor Welded at 666: Buying the Dip as a Structured Trade

July 16, 2026, Thursday. Day five of the chip selloff: TSMC raising its capex outlook somehow lit a fresh round of selling — Micron −8%, my chip name another −5.8%, the index −1.64%, the deepest single day since this scoreboard opened. And one more grenade after the close: the streaming giant reported — EPS beat, next-quarter guidance missed by a breath — down 8% after hours.

I did two things today, and they are two faces of the same coin: in the morning I caught the knife at 708, but in the same minute welded a breakeven floor at 666 under it; in the evening, earnings blew through a put I sold a month ago, and I chose not to dodge — I'll take delivery as contracted. This post is about doing both "buying the dip" and "getting assigned" as structured trades with the mea-culpa price written in before the order goes out.

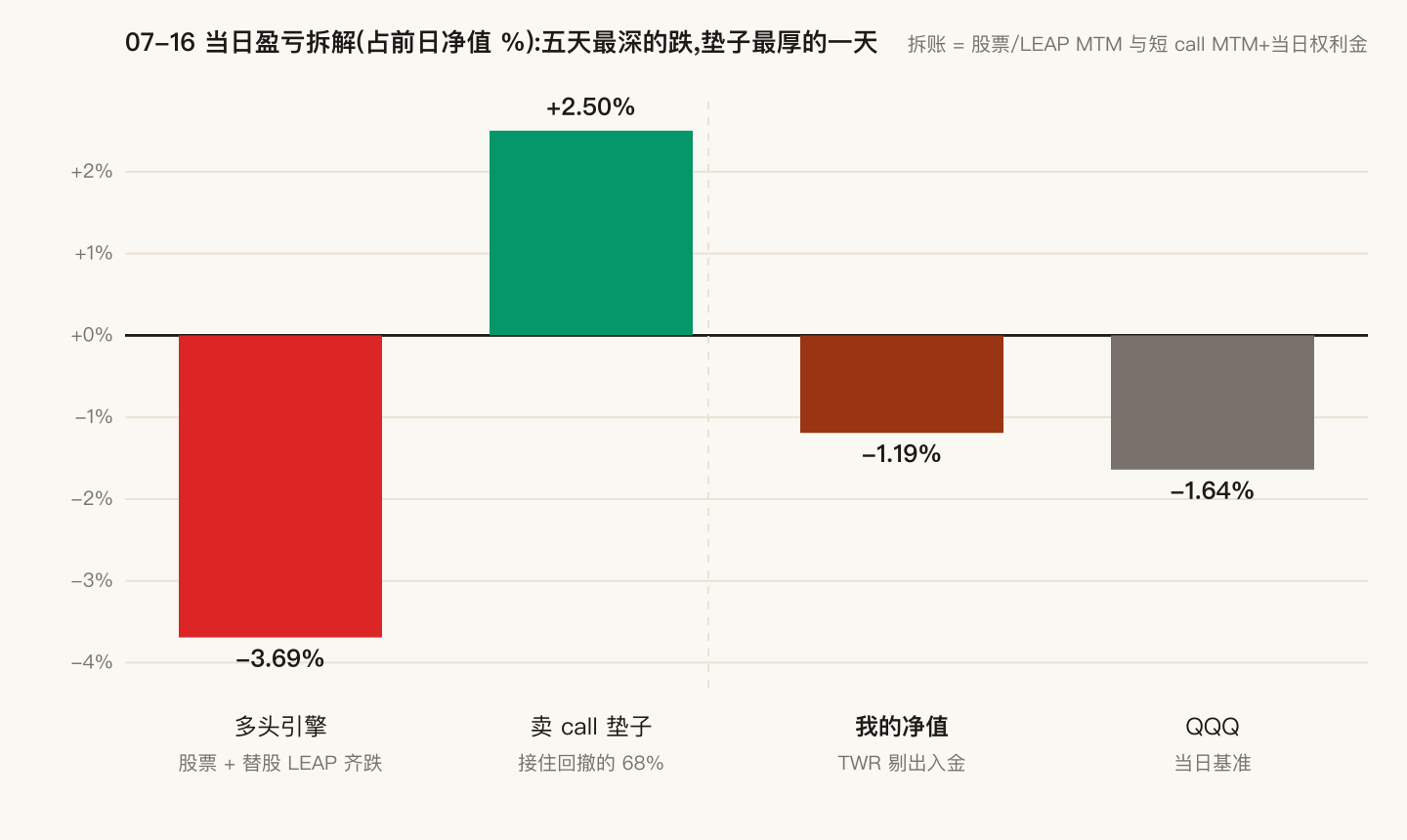

1. The tape: deepest drop, thickest cushion

Index −1.64%, my portfolio −1.19%, ahead by 0.46 points. Decomposed:

Yesterday's post was about paying down debt. Today's first honest sentence: I borrowed part of it back. From the top.

2. The main event: catching the knife with the apology priced in

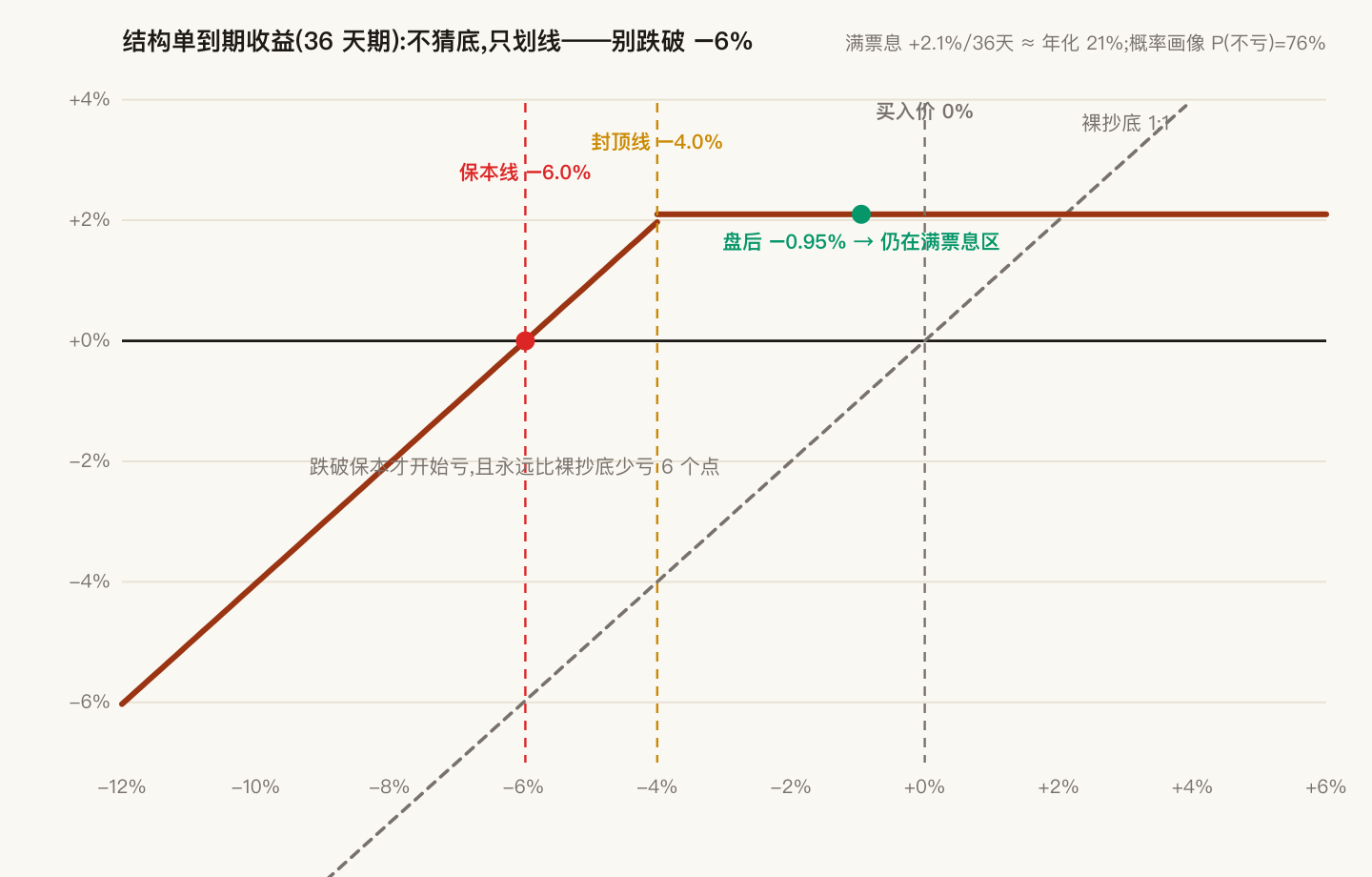

With the index down about 1.3% from the prior close mid-morning, I placed two orders that filled nearly simultaneously:

- Bought an index position a bit over half of net value, filled at 708.31;

- In the same minute sold deep in-the-money calls against all of it — strike 680, 4% below my purchase price, 36 days out, collecting 42.31 per share in premium, about 6% of the purchase price.

This is not "buy the dip and collect some rent on the side." It is one complete structured trade, with three lines drawn before the order went out:

The math deserves to be laid out, because this trade is easily missold as a "high-yield secret," and it isn't. Using the option market's own volatility: about a 76% probability of not losing money at expiry, 67% of collecting the full coupon — but the unconditional expected value annualizes to only around +4%, barely above Treasuries. Option pricing is fair: in the 24% of worlds that go wrong, I ride the index down starting from −6%, and that tail is exactly what eats the expectation. So what this trade buys is not "more return" — it is a different shape of the return distribution: it swaps the most familiar pain in investing, "bought the dip halfway down the mountain," for "three-quarters of the time, a calm 21% annualized."

The very same day ran the first test. The index kept falling after I bought: 708.31 → 705.94 at the close. A naked dip-buy would be down −0.33% at that point; my structure's two legs netted a daily change of 0.00% (stock leg −0.33%, call leg +0.33%). "It kept dropping after I bought" is no longer a sigh — it is this trade's designed operating condition: another 4% down doesn't touch the full coupon, 6% down doesn't touch principal. I don't need to guess the bottom. I only need the index, on August 21, to close no more than 4% below today.

3. The honest ledger on leverage

Yesterday I published "debt stair-stepped from 107% down to 19%." Today's purchase pulled debt back to 69% of net value, and the interest burden from 0.8% back to 2.9% of net value per year. The two posts sit side by side; I won't pretend there's no tension.

My account to myself has three layers. First, what I borrowed back is not naked exposure: the deep ITM calls hedge away about seventy percent of this position's direction, so the portfolio's net directional exposure only rose from 0.7x to 1.1x — the repayment obligation is real; the directional risk is much smaller; keep the two ledgers separate. Second, tomorrow is the month's biggest expiry: of 22 short calls, the lowest strikes sit right at the market — close above and shares auto-deliver to pay down debt; close below and the premium banks in full. The debt valve rings by itself in 24 hours. Third, and most important — last post said the breathing machine manages the shape of exposure, while the size of debt is chosen. Today I chose to borrow size back. That is an active decision the scoreboard gets to judge for a long time, not passive drift. Writing it here is the point.

4. Earnings night: my first delivery

After the close, the streaming giant handed in its paper: EPS beat, revenue and next-quarter guidance a breath short, stock −8% after hours. The 75-strike put I sold a month ago (the lower wing of an iron condor expiring tomorrow) was blown straight through.

Ugly words first: my playbook says close before earnings. The plan to flatten this position slipped from last week to today's session and never executed — earnings are printed on the calendar; this was no black swan. The −6% opening deficit on the delivery is the fine for that delay, logged in the violations ledger.

Then the verdict: no closing — take delivery as contracted. The full sentence behind selling a put was never "collect a little premium." It is "I am willing to buy this company at 75." The market has now handed that sentence back to me verbatim — on a company down 45% from its 2025 peak with earnings still beating. Netting the rent this condor collected, my effective purchase price is around 72, about 6% above the after-hours print; the position is about 6% of net value, inside the 20% single-name limit. Tomorrow night the clearinghouse delivers 1,100 shares at 75 — the same channel as yesterday's post, direction reversed: last time the clearinghouse sold for me; this time it buys for me. No spread, no impact, no commission either way.

The first move after delivery is already written: sell calls against it and start collecting rent. The same assembly line that ground the chip stock's effective cost from 111 to 71 in two months runs again, verbatim.

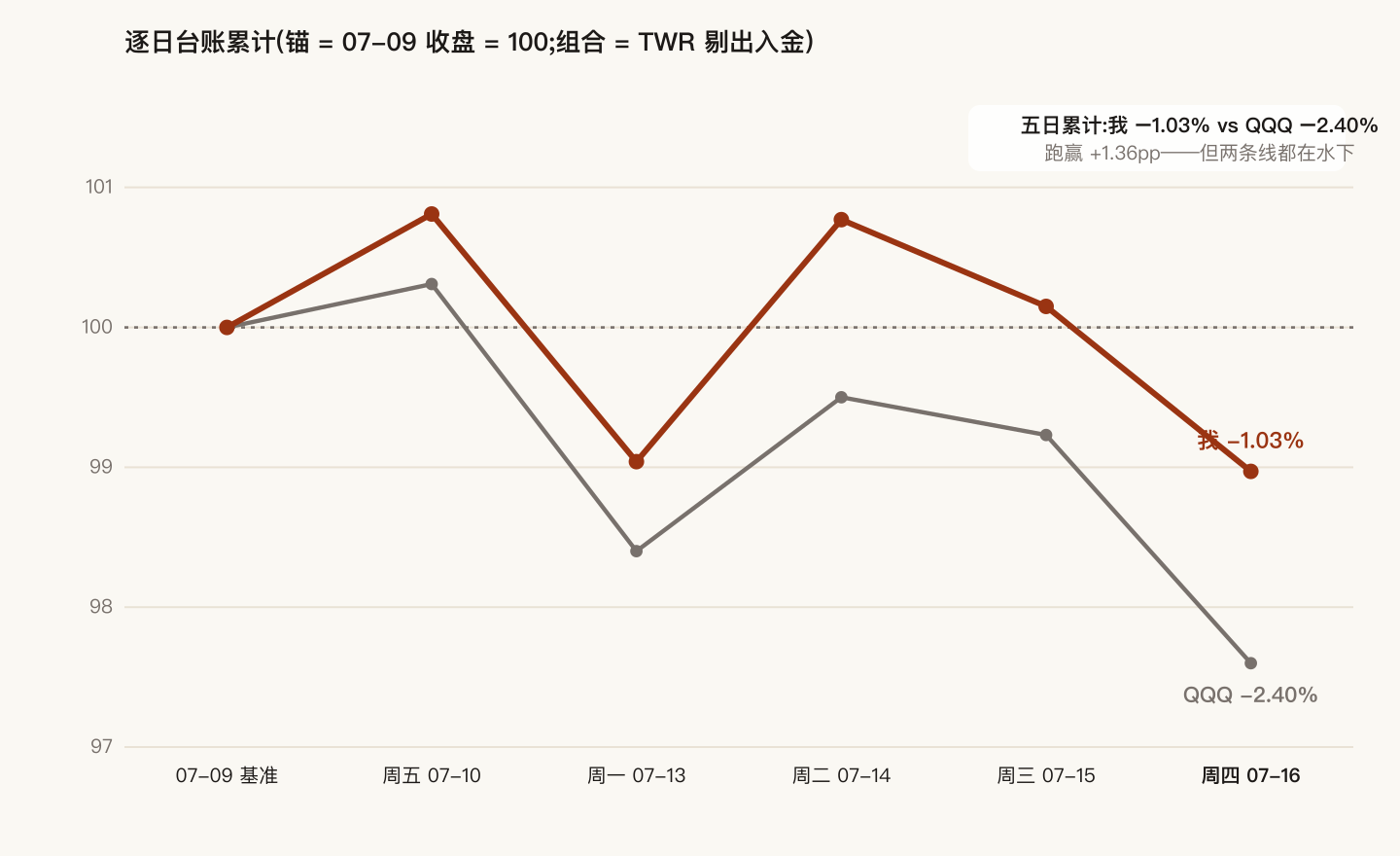

5. Scoreboard: a full week on the books, both lines underwater

The daily ledger continues (anchor = last Thursday's close = 100; portfolio in TWR, deposits excluded):

| Session | Tape | My portfolio | QQQ | Excess |

|---|---|---|---|---|

| Fri 07-10 | chip grinder | +0.81% | +0.31% | +0.50pp |

| Mon 07-13 | more selling | −1.76% | −1.90% | +0.15pp |

| Tue 07-14 | CPI rebound | +1.74% | +1.12% | +0.63pp |

| Wed 07-15 | give-back | −0.60% | −0.27% | −0.33pp |

| Thu 07-16 | deepest of five | −1.19% | −1.64% | +0.46pp |

| 5-day cumulative | one-way whipsaw | −1.03% | −2.40% | +1.36pp |

Tomorrow is Friday, the biggest expiry of the month: 22 index calls await their delivery verdicts, and 1,100 shares of streaming arrive as contracted. The exam is printed; answers tomorrow night.

Last post said the best way to trim is to let the clearinghouse do the selling. This post is its mirror image: the best way to buy a dip is to write the "what if I'm wrong" price into the order before catching the knife. Bought at 708, capped at 680, floored at 666 — all three numbers existed before the order did. Whatever the after-hours tape does, it is testing the structure, not my nerves.

Sources: CNBC — Netflix Q2 2026 earnings: guidance disappoints, stock falls · Yahoo Finance — semiconductors drag indexes lower (July 16, 2026 close) · The Motley Fool — Micron plunges 8% as tech selloff extends (July 16, 2026)